simulate

Monte Carlo simulation of univariate ARIMA or ARIMAX models

Syntax

Description

Y = simulate(Mdl,numobs,Name=Value)simulate returns numeric arrays when all optional input data are

numeric arrays. For example, simulate(Mdl,100,NumPaths=1000,Y0=PS)

returns a numeric array of 1000, 100-period simulated response paths from

Mdl and specifies the numeric array of presample response data

PS.

[

uses any input-argument combination in the previous syntaxes to return numeric arrays of

one or more independent series of model innovations Y,E,V] = simulate(___)E and, when

Mdl represents a composite conditional mean and variance model,

conditional variances V, resulting from simulating the ARIMA

model.

Tbl = simulate(Mdl,numobs,Presample=Presample,PresampleResponseVariable=PresampleResponseVariable)Tbl containing a variable for each of

the random paths of response, innovation, and conditional variance series resulting from

simulating the ARIMA model Mdl. simulate uses

the response variable PresampleResponseVariable in the table or

timetable of presample data Presample to initialize the response

series. (since R2023b)

To initialize the model using presample innovation or conditional variance data,

replace the PresampleResponseVariable name-value argument with

PresampleInnovationVariable or

PresampleVarianceVariable name-value argument.

Tbl = simulate(Mdl,numobs,InSample=InSample,PredictorVariables=PredictorVariables)PredictorVariables in the in-sample table or

timetable of data InSample containing the predictor data for the

exogenous regression component in the ARIMA model Mdl. (since R2023b)

Tbl = simulate(Mdl,numobs,Presample=Presample,PresampleResponseVariable=PresampleResponseVariable,InSample=InSample,PredictorVariables=PredictorVariables)

Tbl = simulate(___,Name=Value)

For example,

simulate(Mdl,100,NumPaths=1000,Presample=PSTbl,PresampleResponseVariables="GDP")

returns a timetable containing a variable for each of the response, innovations, and

conditional variance series. Each variable is a 100-by-1000 matrix representing 1000,

100-period paths simulated from the ARIMA model. simulate

initializes the model by using the presample data in the GDP variable

of the timetable PSTbl.

Examples

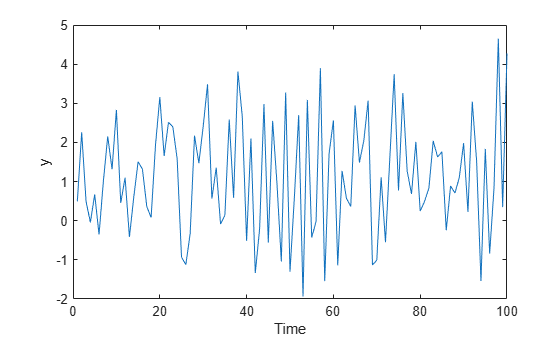

Simulate a response path from an ARIMA model. Return the path in a vector.

Consider the ARIMA(4,1,1) model

where is a Gaussian innovations series with a mean of 0 and a variance of 1.

Create the ARIMA(4,1,1) model.

Mdl = arima(AR=-0.75,ARLags=4,MA=0.1,Constant=2,Variance=1)

Mdl =

arima with properties:

Description: "ARIMA(4,0,1) Model (Gaussian Distribution)"

SeriesName: "Y"

Distribution: Name = "Gaussian"

P: 4

D: 0

Q: 1

Constant: 2

AR: {-0.75} at lag [4]

SAR: {}

MA: {0.1} at lag [1]

SMA: {}

Seasonality: 0

Beta: [1×0]

Variance: 1

Mdl is a fully specified arima object representing the ARIMA(4,1,1) model.

Simulate a 100-period random response path from the ARIMA(4,1,1) model.

rng(1,"twister") % For reproducibility y = simulate(Mdl,100);

y is a 100-by-1 vector containing the random response path.

Plot the simulated path.

plot(y) ylabel("y") xlabel("Time")

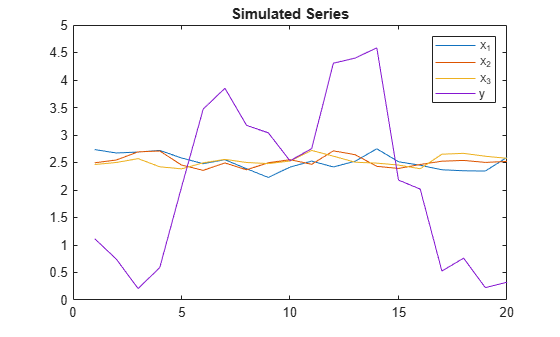

Simulate three predictor series and a response series.

Specify and simulate a path of length 20 for each of the three predictor series modeled by

where follows a Gaussian distribution with mean 0 and variance 0.01, and = {1,2,3}.

[MdlX1,MdlX2,MdlX3] = deal(arima(AR=0.2,MA={0.5 -0.3}, ...

Constant=2,Variance=0.01));

rng(4,"twister"); % For reproducibility

simX1 = simulate(MdlX1,20);

simX2 = simulate(MdlX2,20);

simX3 = simulate(MdlX3,20);

SimX = [simX1 simX2 simX3];Specify and simulate a path of length 20 for the response series modeled by

where follows a Gaussian distribution with mean 0 and variance 1.

MdlY = arima(AR={0.05 -0.02 0.01},MA={0.04 0.01}, ...

D=1,Constant=0.5,Variance=1,Beta=[0.5 -0.03 -0.7]);

simY = simulate(MdlY,20,X=SimX);Plot the series together.

figure plot([SimX simY]) title("Simulated Series") legend("x_1","x_2","x_3","y")

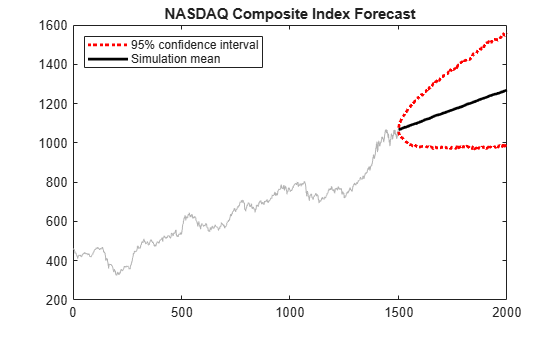

Forecast the daily NASDAQ Composite Index using Monte Carlo simulations. Supply presample observations to initialize the model.

Load the NASDAQ data included with the toolbox. Extract the first 1500 observations for fitting.

load Data_EquityIdx

nasdaq = DataTable.NASDAQ(1:1500);

T = length(nasdaq);Fit an ARIMA(1,1,1) model.

NasdaqModel = arima(1,1,1); NasdaqFit = estimate(NasdaqModel,nasdaq);

ARIMA(1,1,1) Model (Gaussian Distribution):

Value StandardError TStatistic PValue

_________ _____________ __________ __________

Constant 0.43031 0.18555 2.319 0.020393

AR{1} -0.074389 0.081985 -0.90734 0.36422

MA{1} 0.31126 0.077266 4.0284 5.6165e-05

Variance 27.826 0.63625 43.735 0

Simulate 1000 paths with 500 observations each. Use the observed data as presample data.

rng(1,"twister");

Y = simulate(NasdaqFit,500,NumPaths=1000,Y0=nasdaq);Plot the simulation mean forecast and approximate 95% forecast intervals.

lower = prctile(Y,2.5,2); upper = prctile(Y,97.5,2); mn = mean(Y,2); x = T + (1:500); figure plot(nasdaq,Color=[.7,.7,.7]) hold on h1 = plot(x,lower,"r:",LineWidth=2); plot(x,upper,"r:",LineWidth=2) h2 = plot(x,mn,"k",LineWidth=2); legend([h1 h2],"95% confidence interval","Simulation mean", ... Location="NorthWest") title("NASDAQ Composite Index Forecast") hold off

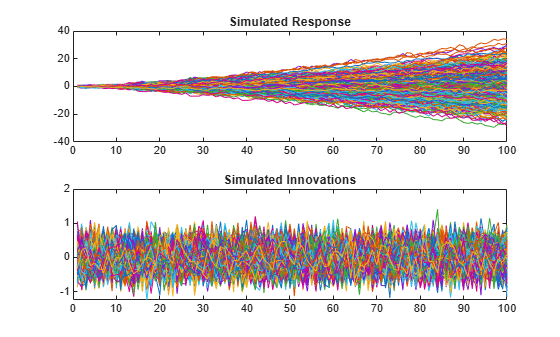

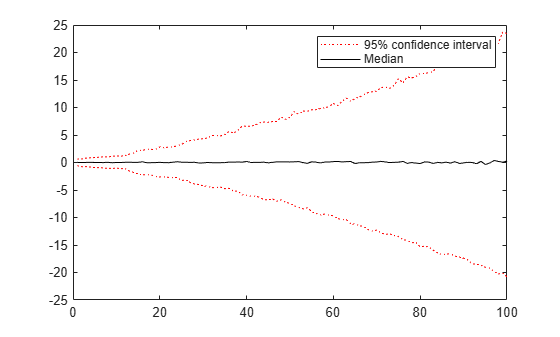

Simulate response and innovation paths from a multiplicative seasonal model.

Specify the model

where follows a Gaussian distribution with mean 0 and variance 0.1.

Mdl = arima(MA=-0.5,SMA=0.3,SMALags=12,D=1, ...

Seasonality=12,Variance=0.1,Constant=0);Simulate 500 paths with 100 observations each.

rng(1,"twister") % For reproducibility [Y,E] = simulate(Mdl,100,NumPaths=500); figure tiledlayout(2,1) nexttile plot(Y) title("Simulated Response") nexttile plot(E) title("Simulated Innovations")

Plot the 2.5th, 50th (median), and 97.5th percentiles of the simulated response paths.

lower = prctile(Y,2.5,2); middle = median(Y,2); upper = prctile(Y,97.5,2); figure plot(1:100,lower,"r:",1:100,middle,"k", ... 1:100,upper,"r:") legend("95% confidence interval","Median")

Compute statistics across the second dimension (across paths) to summarize the sample paths.

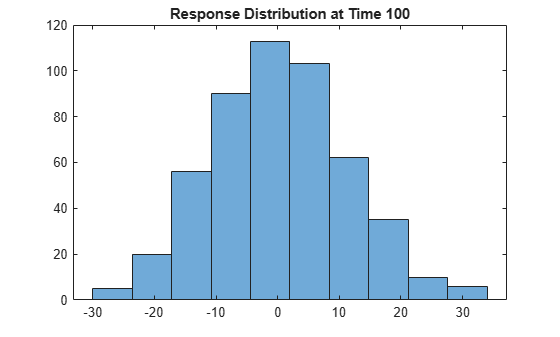

Plot a histogram of the simulated paths at time 100.

figure

histogram(Y(100,:),10)

title("Response Distribution at Time 100")

Fit an ARIMA(1,1,1) model to the weekly average NYSE closing prices. Supply a timetable of presample responses to initialize the model and return a timetable of simulated values from the model.

Load Data

Load the US equity index data set Data_EquityIdx.

load Data_EquityIdx

T = height(DataTimeTable)T = 3028

The timetable DataTimeTable includes the time series variable NYSE, which contains daily NYSE composite closing prices from January 1990 through December 2001.

Plot the daily NYSE price series.

figure

plot(DataTimeTable.Time,DataTimeTable.NYSE)

title("NYSE Daily Closing Prices: 1990 - 2001")

Prepare Timetable for Estimation

When you plan to supply a timetable, you must ensure it has all the following characteristics:

The selected response variable is numeric and does not contain any missing values.

The timestamps in the

Timevariable are regular, and they are ascending or descending.

Remove all missing values from the timetable, relative to the NYSE price series.

DTT = rmmissing(DataTimeTable,DataVariables="NYSE");

T_DTT = height(DTT)T_DTT = 3028

Because all sample times have observed NYSE prices, rmmissing does not remove any observations.

Determine whether the sampling timestamps have a regular frequency and are sorted.

areTimestampsRegular = isregular(DTT,"days")areTimestampsRegular = logical

0

areTimestampsSorted = issorted(DTT.Time)

areTimestampsSorted = logical

1

areTimestampsRegular = 0 indicates that the timestamps of DTT are irregular. areTimestampsSorted = 1 indicates that the timestamps are sorted. Business day rules make daily macroeconomic measurements irregular.

Remedy the time irregularity by computing the weekly average closing price series of all timetable variables.

DTTW = convert2weekly(DTT,Aggregation="mean"); areTimestampsRegular = isregular(DTTW,"weeks")

areTimestampsRegular = logical

1

T_DTTW = height(DTTW)

T_DTTW = 627

DTTW is regular.

figure

plot(DTTW.Time,DTTW.NYSE)

title("NYSE Daily Closing Prices: 1990 - 2001")

Create Model Template for Estimation

Suppose that an ARIMA(1,1,1) model is appropriate to model NYSE composite series during the sample period.

Create an ARIMA(1,1,1) model template for estimation.

Mdl = arima(1,1,1);

Mdl is a partially specified arima model object.

Fit Model to Data

infer requires Mdl.P presample observations to initialize the model. infer backcasts for necessary presample responses, but you can provide a presample.

Partition the data into presample and in-sample, or estimation sample, observations.

T0 = Mdl.P; DTTW0 = DTTW(1:T0,:); DTTW1 = DTTW((T0+1):end,:);

Fit an ARIMA(1,1,1) model to the in-sample weekly average NYSE closing prices. Specify the response variable name, presample timetable, and the presample response variable name.

EstMdl = estimate(Mdl,DTTW1,ResponseVariable="NYSE", ... Presample=DTTW0,PresampleResponseVariable="NYSE");

ARIMA(1,1,1) Model (Gaussian Distribution):

Value StandardError TStatistic PValue

________ _____________ __________ ___________

Constant 0.83623 0.453 1.846 0.064891

AR{1} -0.32862 0.23526 -1.3968 0.16247

MA{1} 0.42702 0.22613 1.8884 0.05897

Variance 56.065 1.8433 30.416 3.3793e-203

EstMdl is a fully specified, estimated arima model object.

Simulate Model

Simulate the fitted model 20 weeks beyond the final period. Specify the entire in-sample data as a presample and the presample response variable name in the in-sample timetable.

rng(1,"twister") % For reproducibility numobs = 20; Tbl = simulate(EstMdl,numobs,Presample=DTTW1, ... PresampleResponseVariable="NYSE"); tail(Tbl)

Time Y_Response Y_Innovation Y_Variance

___________ __________ ____________ __________

05-Apr-2002 564.68 -11.302 56.065

12-Apr-2002 570.47 6.5582 56.065

19-Apr-2002 570.39 -1.8179 56.065

26-Apr-2002 571.72 1.249 56.065

03-May-2002 557.94 -14.716 56.065

10-May-2002 547.51 -9.5098 56.065

17-May-2002 556.51 8.7992 56.065

24-May-2002 573.34 15.194 56.065

size(Tbl)

ans = 1×2

20 3

Tbl is a 20-by-3 timetable containing the simulated response path NYSE_Response, the corresponding simulated innovation path NYSE_Innovation, and the constant variance path NYSE_Variance (Mdl.Variance = 56.065).

Plot the simulated responses.

figure plot(DTTW1.Time((end-50):end),DTTW1.NYSE((end-50):end), ... Color=[0.7 0.7 0.7],LineWidth=2); hold on plot(Tbl.Time,Tbl.Y_Response,LineWidth=2); legend("Observed","Simulated responses") title("Weekly Average NYSE CLosing Prices") hold off

Fit an ARIMAX(1,1,1) model to the weekly average NYSE closing prices. Include an exogenous regression term identifying whether a measurement observation occurs during a recession. Supply timetables of presample and in-sample exogenous data. Simulate the weekly average closing prices over a 10-week horizon, and compare the forecasts to held out data.

Load the US equity index data set Data_EquityIdx.

load Data_EquityIdx

T = height(DataTimeTable)T = 3028

Remedy the time irregularity by computing the weekly average closing price series of all timetable variables.

DTTW = convert2weekly(DataTimeTable,Aggregation="mean");

T_DTTW = height(DTTW)T_DTTW = 627

Load the US recessions data set.

load Data_Recessions RDT = datetime(Recessions,ConvertFrom="datenum", ... Format="yyyy-MM-dd");

Determine whether each sampling time in the data occurs during a US recession.

isrecession = @(x)any(isbetween(x,RDT(:,1),RDT(:,2))); DTTW.IsRecession = arrayfun(isrecession,DTTW.Time)*1;

DTTW contains a variable IsRecession, which represents the exogenous variable in the ARIMAX model.

Create an ARIMA(1,1,1) model template for estimation. Set the response series name to NYSE.

Mdl = arima(1,1,1);

Mdl.SeriesName = "NYSE";Partition the data into required presample, in-sample (estimation sample), and 10 holdout sample observations.

T0 = Mdl.P; T2 = 10; DTTW0 = DTTW(1:T0,:); DTTW1 = DTTW((T0+1):(end-T2),:); DTTW2 = DTTW((end-T2+1):end,:);

Fit an ARIMA(1,1,1) model to the in-sample weekly average NYSE closing prices. Specify the presample timetable, the presample response variable name, and the in-sample predictor variable name.

EstMdl = estimate(Mdl,DTTW1,Presample=DTTW0,PresampleResponseVariable="NYSE", ... PredictorVariables="IsRecession");

ARIMAX(1,1,1) Model (Gaussian Distribution):

Value StandardError TStatistic PValue

________ _____________ __________ ___________

Constant 1.0635 0.50013 2.1264 0.033469

AR{1} -0.33827 0.2088 -1.6201 0.10521

MA{1} 0.43879 0.20045 2.189 0.028596

Beta(1) -2.425 1.0861 -2.2327 0.02557

Variance 55.527 1.9255 28.838 7.0977e-183

Simulate 1000 paths of responses from the fitted model into a 10-week horizon. Specify the in-sample data as a presample, the presample response variable name, the predictor data in the forecast horizon, and the predictor variable name.

rng(1,"twister") Tbl = simulate(EstMdl,T2,Presample=DTTW1,PresampleResponseVariable="NYSE", ... InSample=DTTW2,PredictorVariables="IsRecession",NumPaths=1000);

Tbl is a 10-by-6 timetable containing all variables in InSample, and the following variables:

NYSE_Response: a 10-by-1000 matrix of 1000 random response paths simulated from the model.NYSE_Innovation: a 10-by-1000 matrix of 1000 random innovation paths filtered through the model to product the response pathsNYSE_Variance: a 10-by-1000 matrix containing only the constantMdl.Variance = 55.527.

Plot the observed responses, median of the simulated responses, a 95% percentile intervals of the simulated values.

SimStats = quantile(Tbl.NYSE_Response,[0.025 0.5 0.975],2); figure h1 = plot(DTTW.Time((end-50):end),DTTW.NYSE((end-50):end),"k",LineWidth=2); hold on plot(Tbl.Time,Tbl.NYSE_Response,Color=[0.8 0.8 0.8]) h2 = plot(Tbl.Time,SimStats(:,2),'r--'); h3 = plot(Tbl.Time,SimStats(:,[1 3]),'b--'); legend([h1 h2 h3(1)],["Observations" "Sim. medians" "95% percentile intervals"]) title("NYSE Weekly Average Price Series and Monte Carlo Forecasts")

Input Arguments

Name-Value Arguments

Output Arguments

References

[1] Box, George E. P., Gwilym M. Jenkins, and Gregory C. Reinsel. Time Series Analysis: Forecasting and Control. 3rd ed. Englewood Cliffs, NJ: Prentice Hall, 1994.

[2] Enders, Walter. Applied Econometric Time Series. Hoboken, NJ: John Wiley & Sons, Inc., 1995.

[3] Hamilton, James D. Time Series Analysis. Princeton, NJ: Princeton University Press, 1994.

Version History

Introduced in R2012aSee Also

Objects

Functions

Topics

- Simulate Stationary Processes

- Simulate Trend-Stationary and Difference-Stationary Processes

- Simulate Seasonal ARIMA (SARIMA) Models

- Simulate Conditional Mean and Variance Models

- Monte Carlo Simulation of Conditional Mean Models

- Presample Data for Conditional Mean Model Simulation

- Transient Effects in Conditional Mean Model Simulations

- Forecast Conditional Mean Model Programmatically