FixedBond

FixedBond instrument object

Description

Create and price a FixedBond instrument object for one of

more Fixed Bond instruments using this workflow:

Use

fininstrumentto create aFixedBondinstrument object for one of more Fixed Bond instruments.Use

ratecurveto specify a curve model for theFixedBondinstrument object or use aHullWhite,BlackKarasinski,BlackDermanToy,BraceGatarekMusiela,SABRBraceGatarekMusiela,CoxIngersollRoss, orLinearGaussian2Fmodel.Choose a pricing method.

When using a

ratecurveusefinpricerto specify aDiscountpricing method for one or moreFixedBondinstruments.When using a

HullWhite,BlackKarasinski,CoxIngersollRoss, orBlackDermanToymodel, usefinpricerto specify anIRTreepricing method for one or moreFixedBondinstruments.When using a

HullWhite,BlackKarasinski,BraceGatarekMusiela,SABRBraceGatarekMusiela, orLinearGaussian2Fmodel, usefinpricerto specify anIRMonteCarlopricing method for one or moreFixedBondinstruments.

For more detailed information on this workflow, see Get Started with Workflows Using Object-Based Framework for Pricing Financial Instruments.

For more information on the available models and pricing methods for a

FixedBond instrument, see Choose Instruments, Models, and Pricers.

Creation

Syntax

Description

FixedBondObj = fininstrument(InstrumentType,'CouponRate',couponrate_value,'Maturity',maturity_date)FixedBond object for one of more Fixed Bond

instruments by specifying InstrumentType and sets the

properties for the

required name-value pair arguments CouponRate and

Maturity.

The FixedBond instrument supports a vanilla bond, a

stepped coupon bond, and an amortizing bond. For more information, see More About.

FixedBondObj = fininstrument(___,Name,Value)FixedBondObj =

fininstrument("FixedBond",'CouponRate',0.34,'Maturity',datetime(2019,1,30),'Period',4,'Basis',1,'Principal',100,'FirstCouponDate',datetime(2016,1,30),'EndMonthRule',true,'Name',"fixedbond_instrument")

creates a FixedBond option with a coupon rate of 0.34 and

a maturity of January 30, 2019. You can specify multiple name-value pair

arguments.

Input Arguments

Name-Value Arguments

Output Arguments

Properties

Object Functions

cashflows | Compute cash flow for FixedBond, FloatBond,

Swap, FRA, STIRFuture,

OISFuture, OvernightIndexedSwap, or

Deposit instrument |

Examples

This example shows the workflow to price a vanilla FixedBond instrument when you use a ratecurve and a Discount pricing method.

Create FixedBond Instrument Object

Use fininstrument to create a FixedBond instrument object.

FixB = fininstrument("FixedBond",'Maturity',datetime(2022,9,15),'CouponRate',0.021,'Period',2,'Basis',1,'Principal',100,'Name',"fixed_bond_instrument")

FixB =

FixedBond with properties:

CouponRate: 0.0210

Period: 2

Basis: 1

EndMonthRule: 1

Principal: 100

DaycountAdjustedCashFlow: 0

BusinessDayConvention: "actual"

Holidays: NaT

IssueDate: NaT

FirstCouponDate: NaT

LastCouponDate: NaT

StartDate: NaT

Maturity: 15-Sep-2022

Name: "fixed_bond_instrument"

Create ratecurve Object

Create a ratecurve object using ratecurve.

Settle = datetime(2018,9,15); Type = 'zero'; ZeroTimes = [calmonths(6) calyears([1 2 3 4 5 7 10 20 30])]'; ZeroRates = [0.0052 0.0055 0.0061 0.0073 0.0094 0.0119 0.0168 0.0222 0.0293 0.0307]'; ZeroDates = Settle + ZeroTimes; myRC = ratecurve('zero',Settle,ZeroDates,ZeroRates)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 0

Dates: [10×1 datetime]

Rates: [10×1 double]

Settle: 15-Sep-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create Discount Pricer Object

Use finpricer to create a Discount pricer object and use the ratecurve object with the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("Discount",'DiscountCurve',myRC)

outPricer =

Discount with properties:

DiscountCurve: [1×1 ratecurve]

Price FixedBond Instrument

Use price to compute the price and sensitivities for the FixedBond instrument.

[Price, outPR] = price(outPricer, FixB,["all"])Price = 104.5679

outPR =

priceresult with properties:

Results: [1×2 table]

PricerData: []

outPR.Results

ans=1×2 table

Price DV01

______ ________

104.57 0.040397

This example shows how to create a FixedBond instrument and then use any of the following Financial Toolbox™ functions to perform bond analytics: bnddurp, bnddury, bndconvp, bndconvy, bndkrdur, cfdur, and cfconv.

Create FixedBond Instrument Object

Use fininstrument to create a FixedBond instrument object.

MaturityDate = datetime(2027,12,16); CouponRate = 0.01; FixedBondObj = fininstrument('FixedBond','CouponRate',CouponRate,'Maturity',MaturityDate);

Create ratecurve Object

Create a ratecurve object using ratecurve.

Settle = datetime(2022,10,10);

MarketDates = datetime([2023,9,15 ; 2024,9,15 ; 2025,9,15 ; 2026,9,15 ; 2027,9,15 ; 2028,9,15]);

ZeroDates = datetime([2023,10,15 ; 2024,10,15 ; 2025,10,15 ; 2026,10,15 ; 2027,10,15 ; 2028,10,15]);

ZeroRates = [4.2520 4.1081 3.8801 3.7170 3.6060 3.5250]'/100;

MarketSpreads = [97.9825 97.9825 97.9825 97.9825 97.9825 97.9825]';

RateObjB = ratecurve('zero',Settle,ZeroDates,ZeroRates+MarketSpreads(1)/10000); Create Discount Pricer Object

Use finpricer to create a Discount pricer object and use the ratecurve object with the 'DiscountCurve' name-value argument.

Pricer1 = finpricer("Discount",'DiscountCurve',RateObjB);

Price FixedBond Instrument

Use price to compute the price and sensitivities for the FixedBond instrument.

[Price1, outPR] = price(Pricer1, FixedBondObj,["all"])Price1 = 83.4210

outPR =

priceresult with properties:

Results: [1×2 table]

PricerData: []

Compute Bond Durations for FixedBond Instrument

Use bnddurp to compute the bond durations given the bond price.

[ModDuration, YearDuration, PerDuration] = bnddurp(Price1,FixedBondObj.CouponRate, Settle, FixedBondObj.Maturity,Period=FixedBondObj.Period)

ModDuration = 4.9169

YearDuration = 5.0308

PerDuration = 10.0616

Compute Key Rate Durations for FixedBond Instrument

Use bndkrdur to compute the FixedBond instrument key rate duration given a zero curve.

ZeroData1 = [datenum(RateObjB.Dates) RateObjB.Rates]; KeyRateDuration = bndkrdur(ZeroData1,FixedBondObj.CouponRate,Settle,FixedBondObj.Maturity)

KeyRateDuration = 1×6

0.0133 0.0212 0.0304 0.0389 4.0226 0.8164

This example shows the workflow to price multiple vanilla FixedBond instruments when you use a ratecurve and a Discount pricing method.

Create FixedBond Instrument Object

Use fininstrument to create a FixedBond instrument object for three Fixed Bond instruments.

FixB = fininstrument("FixedBond",'Maturity',datetime([2022,9,15 ; 2022,10,15 ; 2022,11,15]),'CouponRate',0.021,'Period',2,'Basis',1,'Principal',[100 ; 250 ; 500],'Name',"fixed_bond_instrument")

FixB=3×1 FixedBond array with properties:

CouponRate

Period

Basis

EndMonthRule

Principal

DaycountAdjustedCashFlow

BusinessDayConvention

Holidays

IssueDate

FirstCouponDate

LastCouponDate

StartDate

Maturity

Name

Create ratecurve Object

Create a ratecurve object using ratecurve.

Settle = datetime(2018,9,15); Type = 'zero'; ZeroTimes = [calmonths(6) calyears([1 2 3 4 5 7 10 20 30])]'; ZeroRates = [0.0052 0.0055 0.0061 0.0073 0.0094 0.0119 0.0168 0.0222 0.0293 0.0307]'; ZeroDates = Settle + ZeroTimes; myRC = ratecurve('zero',Settle,ZeroDates,ZeroRates)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 0

Dates: [10×1 datetime]

Rates: [10×1 double]

Settle: 15-Sep-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create Discount Pricer Object

Use finpricer to create a Discount pricer object and use the ratecurve object with the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("Discount",'DiscountCurve',myRC)

outPricer =

Discount with properties:

DiscountCurve: [1×1 ratecurve]

Price FixedBond Instruments

Use price to compute the prices and sensitivities for the FixedBond instruments.

[Price, outPR] = price(outPricer, FixB,["all"])Price = 3×1

104.5679

261.4498

522.9174

outPR=1×3 priceresult array with properties:

Results

PricerData

outPR.Results

ans=1×2 table

Price DV01

______ ________

104.57 0.040397

ans=1×2 table

Price DV01

______ _____

261.45 0.103

ans=1×2 table

Price DV01

______ _______

522.92 0.21013

This example shows the workflow to price a stepped FixedBond instrument when you use a ratecurve and a Discount pricing method.

Create FixedBond Instrument Object

Use fininstrument to create a stepped FixedBond instrument object.

Maturity = datetime(2024,1,1); Period = 1; CDates = datetime([2020,1,1 ; 2024,1,1]); CRates = [.025; .03]; CouponRate = timetable(CDates,CRates); SBond = fininstrument("FixedBond",'Maturity',Maturity,'CouponRate',CouponRate,'Period',Period)

SBond =

FixedBond with properties:

CouponRate: [2×1 timetable]

Period: 1

Basis: 0

EndMonthRule: 1

Principal: 100

DaycountAdjustedCashFlow: 0

BusinessDayConvention: "actual"

Holidays: NaT

IssueDate: NaT

FirstCouponDate: NaT

LastCouponDate: NaT

StartDate: NaT

Maturity: 01-Jan-2024

Name: ""

Create ratecurve Object

Create a ratecurve object using ratecurve.

Settle = datetime(2018,1,1); ZeroTimes = calyears(1:10)'; ZeroRates = [0.0052 0.0055 0.0061 0.0073 0.0094 0.0119 0.0168 0.0222 0.0293 0.0307]'; ZeroDates = Settle + ZeroTimes; Compounding = 1; ZeroCurve = ratecurve("zero",Settle,ZeroDates,ZeroRates, "Compounding",Compounding)

ZeroCurve =

ratecurve with properties:

Type: "zero"

Compounding: 1

Basis: 0

Dates: [10×1 datetime]

Rates: [10×1 double]

Settle: 01-Jan-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create Discount Pricer Object

Use finpricer to create a Discount pricer object and use the ratecurve object with the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("Discount",'DiscountCurve',ZeroCurve)

outPricer =

Discount with properties:

DiscountCurve: [1×1 ratecurve]

Price FixedBond Instrument

Use price to compute the price and sensitivities for the vanilla FixedBond instrument.

[Price, outPR] = price(outPricer, SBond,["all"])Price = 109.6218

outPR =

priceresult with properties:

Results: [1×2 table]

PricerData: []

outPR.Results

ans=1×2 table

Price DV01

______ ________

109.62 0.061108

This example shows the workflow to price an amortizing FixedBond instrument when you use a ratecurve and a Discount pricing method.

Create FixedBond Instrument Object

Use fininstrument to create an amortizing FixedBond instrument object.

Maturity = datetime(2024,1,1); Period = 1; ADates = datetime([2020,1,1 ; 2024,1,1]); APrincipal = [100; 85]; Principal = timetable(ADates,APrincipal); Bondamort = fininstrument("FixedBond",'Maturity',Maturity,'CouponRate',0.025,'Period',Period,'Principal',Principal)

Bondamort =

FixedBond with properties:

CouponRate: 0.0250

Period: 1

Basis: 0

EndMonthRule: 1

Principal: [2×1 timetable]

DaycountAdjustedCashFlow: 0

BusinessDayConvention: "actual"

Holidays: NaT

IssueDate: NaT

FirstCouponDate: NaT

LastCouponDate: NaT

StartDate: NaT

Maturity: 01-Jan-2024

Name: ""

Create ratecurve Object

Create a ratecurve object using ratecurve.

Settle = datetime(2018,1,1); ZeroTimes = calyears(1:10)'; ZeroRates = [0.0052 0.0055 0.0061 0.0073 0.0094 0.0119 0.0168 0.0222 0.0293 0.0307]'; ZeroDates = Settle + ZeroTimes; Compounding = 1; ZeroCurve = ratecurve("zero",Settle,ZeroDates,ZeroRates, "Compounding",Compounding);

Create Discount Pricer Object

Use finpricer to create a Discount pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("Discount",'DiscountCurve',ZeroCurve)

outPricer =

Discount with properties:

DiscountCurve: [1×1 ratecurve]

Price FixedBond Instrument

Use price to compute the price and sensitivities for the vanilla FixedBond instrument.

[Price, outPR] = price(outPricer,Bondamort,["all"])Price = 107.1273

outPR =

priceresult with properties:

Results: [1×2 table]

PricerData: []

outPR.Results

ans=1×2 table

Price DV01

______ ________

107.13 0.054279

This example shows the workflow to price a FixedBond instrument when using a HullWhite model and an IRMonteCarlo pricing method.

Create FixedBond Instrument Object

Use fininstrument to create a FixedBond instrument object.

FixB = fininstrument("FixedBond","Maturity",datetime(2022,9,15),"CouponRate",0.05,'Name',"fixed_bond")

FixB =

FixedBond with properties:

CouponRate: 0.0500

Period: 2

Basis: 0

EndMonthRule: 1

Principal: 100

DaycountAdjustedCashFlow: 0

BusinessDayConvention: "actual"

Holidays: NaT

IssueDate: NaT

FirstCouponDate: NaT

LastCouponDate: NaT

StartDate: NaT

Maturity: 15-Sep-2022

Name: "fixed_bond"

Create HullWhite Model Object

Use finmodel to create a HullWhite model object.

HullWhiteModel = finmodel("HullWhite",'Alpha',0.32,'Sigma',0.49)

HullWhiteModel =

HullWhite with properties:

Alpha: 0.3200

Sigma: 0.4900

Create ratecurve Object

Create a ratecurve object using ratecurve.

Settle = datetime(2019,1,1); Type = 'zero'; ZeroTimes = [calmonths(6) calyears([1 2 3 4 5 7 10 20 30])]'; ZeroRates = [0.0052 0.0055 0.0061 0.0073 0.0094 0.0119 0.0168 0.0222 0.0293 0.0307]'; ZeroDates = Settle + ZeroTimes; myRC = ratecurve('zero',Settle,ZeroDates,ZeroRates)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 0

Dates: [10×1 datetime]

Rates: [10×1 double]

Settle: 01-Jan-2019

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create IRMonteCarlo Pricer Object

Use finpricer to create an IRMonteCarlo pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("IRMonteCarlo",'Model',HullWhiteModel,'DiscountCurve',myRC,'SimulationDates',ZeroDates)

outPricer =

HWMonteCarlo with properties:

NumTrials: 1000

RandomNumbers: []

DiscountCurve: [1×1 ratecurve]

SimulationDates: [01-Jul-2019 01-Jan-2020 01-Jan-2021 01-Jan-2022 01-Jan-2023 01-Jan-2024 01-Jan-2026 01-Jan-2029 01-Jan-2039 01-Jan-2049]

Model: [1×1 finmodel.HullWhite]

Price FixedBond Instrument

Use price to compute the price and sensitivities for the FixedBond instrument.

[Price,outPR] = price(outPricer,FixB,["all"])Price = 115.0303

outPR =

priceresult with properties:

Results: [1×4 table]

PricerData: [1×1 struct]

outPR.Results

ans=1×4 table

Price Delta Gamma Vega

______ _______ ______ ____

115.03 -397.13 1430.4 0

This example shows the workflow to price a FixedBond instrument when using a HullWhite model and a IRTree pricing method.

Create FixedBond Instrument Object

Use fininstrument to create a FixedBond instrument object.

FixB = fininstrument("FixedBond","Maturity",datetime(2029,9,15),"CouponRate",.05,"Period",1,"Name","fixed_bond_instrument")

FixB =

FixedBond with properties:

CouponRate: 0.0500

Period: 1

Basis: 0

EndMonthRule: 1

Principal: 100

DaycountAdjustedCashFlow: 0

BusinessDayConvention: "actual"

Holidays: NaT

IssueDate: NaT

FirstCouponDate: NaT

LastCouponDate: NaT

StartDate: NaT

Maturity: 15-Sep-2029

Name: "fixed_bond_instrument"

Create ratecurve Object

Create a ratecurve object using ratecurve.

Settle = datetime(2019,9,15); Type = "zero"; ZeroTimes = [calyears([1:10])]'; ZeroRates = [0.0055 0.0061 0.0073 0.0094 0.0119 0.0168 0.0222 0.0293 0.0307 0.0310]'; ZeroDates = Settle + ZeroTimes; myRC = ratecurve('zero',Settle,ZeroDates,ZeroRates)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 0

Dates: [10×1 datetime]

Rates: [10×1 double]

Settle: 15-Sep-2019

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create HullWhite Model Object

Use finmodel to create a HullWhite model object.

HullWhiteModel = finmodel("hullwhite",'Alpha',0.052,'Sigma',0.34)

HullWhiteModel =

HullWhite with properties:

Alpha: 0.0520

Sigma: 0.3400

Create IRTree Pricer Object

Use finpricer to create an IRTree pricer object and use the ratecurve object with the 'DiscountCurve' name-value pair argument.

HWTreePricer = finpricer("irtree","model",HullWhiteModel,"DiscountCurve",myRC,"TreeDates",ZeroDates)

HWTreePricer =

HWBKTree with properties:

Tree: [1×1 struct]

TreeDates: [10×1 datetime]

Model: [1×1 finmodel.HullWhite]

DiscountCurve: [1×1 ratecurve]

HWTreePricer.Tree

ans = struct with fields:

tObs: [0 1 1.9973 2.9945 3.9918 4.9918 5.9891 6.9863 7.9836 8.9836]

dObs: [15-Sep-2019 15-Sep-2020 15-Sep-2021 15-Sep-2022 15-Sep-2023 15-Sep-2024 15-Sep-2025 15-Sep-2026 15-Sep-2027 15-Sep-2028]

CFlowT: {[10×1 double] [9×1 double] [8×1 double] [7×1 double] [6×1 double] [5×1 double] [4×1 double] [3×1 double] [2×1 double] [9.9809]}

Probs: {[3×1 double] [3×3 double] [3×5 double] [3×7 double] [3×9 double] [3×11 double] [3×13 double] [3×15 double] [3×17 double]}

Connect: {[2] [2 3 4] [2 3 4 5 6] [2 3 4 5 6 7 8] [2 3 4 5 6 7 8 9 10] [2 3 4 5 6 7 8 9 10 11 12] [2 3 4 5 6 7 8 9 10 11 12 13 14] [2 3 4 5 6 7 8 9 10 11 12 13 14 15 16] [2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18]}

FwdTree: {1×10 cell}

RateTree: {1×10 cell}

Price FixedBond Instrument

Use price to compute the price and sensitivities for the FixedBond instrument.

[Price, outPR] = price(HWTreePricer, FixB,["all"])Price = 117.9440

outPR =

priceresult with properties:

Results: [1×4 table]

PricerData: [1×1 struct]

outPR.Results

ans=1×4 table

Price Delta Gamma Vega

______ _______ ______ ___________

117.94 -964.01 8868.6 -4.2633e-10

This example shows the workflow to price a FixedBond instrument when you use a CoxIngersollRoss model and an IRTree pricing method.

Create FixedBond Instrument Object

Use fininstrument to create a FixedBond instrument object.

Period = 1; Maturity = datetime(2027,1,1); CouponRate = 0.035; FixedBond = fininstrument("FixedBond",'Maturity',Maturity,'CouponRate',CouponRate,'Period',Period,Name="fixed_bond")

FixedBond =

FixedBond with properties:

CouponRate: 0.0350

Period: 1

Basis: 0

EndMonthRule: 1

Principal: 100

DaycountAdjustedCashFlow: 0

BusinessDayConvention: "actual"

Holidays: NaT

IssueDate: NaT

FirstCouponDate: NaT

LastCouponDate: NaT

StartDate: NaT

Maturity: 01-Jan-2027

Name: "fixed_bond"

Create CoxIngersollRoss Model Object

Use finmodel to create a CoxIngersollRoss model object.

alpha = 0.03;

theta = 0.02;

sigma = 0.1;

CIRModel = finmodel("CoxIngersollRoss",Sigma=sigma,Alpha=alpha,Theta=theta)CIRModel =

CoxIngersollRoss with properties:

Sigma: 0.1000

Alpha: 0.0300

Theta: 0.0200

Create ratecurve Object

Create a ratecurve object using ratecurve.

Times= [calyears([1 2 3 4 ])]';

Settle = datetime(2023,1,1);

ZRates = [0.035; 0.042147; 0.047345; 0.052707]';

ZDates = Settle + Times;

Compounding = -1;

Basis = 1;

ZeroCurve = ratecurve("zero",Settle,ZDates,ZRates,Compounding = Compounding, Basis = Basis);Create IRTree Pricer Object

Use finpricer to create an IRTree pricer object for the CoxIngersollRoss model and use the ratecurve object for the 'DiscountCurve' name-value argument.

CIRPricer = finpricer("irtree",Model=CIRModel,DiscountCurve=ZeroCurve,Maturity=ZDates(end),NumPeriods=length(ZDates))CIRPricer =

CIRTree with properties:

Tree: [1×1 struct]

TreeDates: [4×1 datetime]

Model: [1×1 finmodel.CoxIngersollRoss]

DiscountCurve: [1×1 ratecurve]

Price FixedBond Instrument

Use price to compute the price for the FixedBond instrument.

[Price,outPR] = price(CIRPricer,FixedBond,"all")Price = 93.4593

outPR =

priceresult with properties:

Results: [1×4 table]

PricerData: [1×1 struct]

outPR.Results

ans=1×4 table

Price Delta Gamma Vega

______ _______ ______ ___________

93.459 -354.23 1384.8 -1.4211e-10

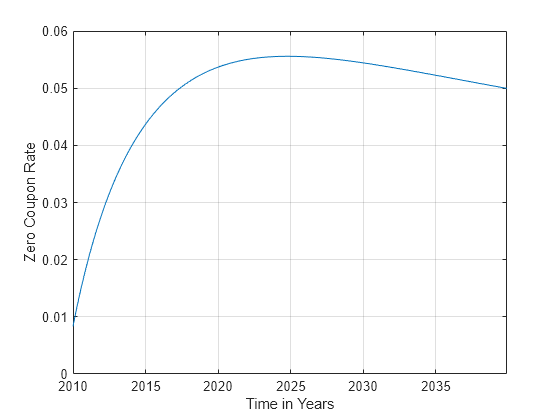

This example shows the workflow for using FixedBond instruments that are fit to a Svensson model using fitSvensson.

Define the bond data and use fininstrument to create FixedBond instrument objects.

settle = datetime(2009,11,24)

settle = datetime

24-Nov-2009

maturity = settle + calyears([1;2;3;5;7;10;20;30])

maturity = 8×1 datetime

24-Nov-2010

24-Nov-2011

24-Nov-2012

24-Nov-2014

24-Nov-2016

24-Nov-2019

24-Nov-2029

24-Nov-2039

price = [100.1; 100.1; 100.2; 99.0; ... 100.8; 99.2; 101.7; 100.2]; coupon = [0.020; 0.0275; 0.035; 0.042; ... 0.0475; 0.0525; 0.055; 0.052]; Bonds = fininstrument("FixedBond",'Maturity',maturity,'CouponRate',coupon)

Bonds=8×1 FixedBond array with properties:

CouponRate

Period

Basis

EndMonthRule

Principal

DaycountAdjustedCashFlow

BusinessDayConvention

Holidays

IssueDate

FirstCouponDate

LastCouponDate

StartDate

Maturity

Name

Use fitSvensson to create a parameter curve object.

lb = [-Inf -Inf -Inf -Inf 0 0]; ub = [Inf Inf Inf Inf 5 20]; x0 = [.5 .5 .5 .5 2 5]; SvenModel = fitSvensson(settle,Bonds,price,'x0',x0,'lb',lb,'ub',ub)

Local minimum possible. lsqnonlin stopped because the final change in the sum of squares relative to its initial value is less than the value of the function tolerance. <stopping criteria details>

SvenModel =

parametercurve with properties:

Type: "zero"

Settle: 24-Nov-2009

Compounding: -1

Basis: 0

FunctionHandle: @(t)fitF(Params,t)

Parameters: [0.0290 -0.0217 0.0024 0.0973 1.7779 7.5287]

p = SvenModel.Parameters

p = 1×6

0.0290 -0.0217 0.0024 0.0973 1.7779 7.5287

maturities = settle(1) + calmonths(1:360)

maturities = 1×360 datetime

24-Dec-2009 24-Jan-2010 24-Feb-2010 24-Mar-2010 24-Apr-2010 24-May-2010 24-Jun-2010 24-Jul-2010 24-Aug-2010 24-Sep-2010 24-Oct-2010 24-Nov-2010 24-Dec-2010 24-Jan-2011 24-Feb-2011 24-Mar-2011 24-Apr-2011 24-May-2011 24-Jun-2011 24-Jul-2011 24-Aug-2011 24-Sep-2011 24-Oct-2011 24-Nov-2011 24-Dec-2011 24-Jan-2012 24-Feb-2012 24-Mar-2012 24-Apr-2012 24-May-2012 24-Jun-2012 24-Jul-2012 24-Aug-2012 24-Sep-2012 24-Oct-2012 24-Nov-2012 24-Dec-2012 24-Jan-2013 24-Feb-2013 24-Mar-2013 24-Apr-2013 24-May-2013 24-Jun-2013 24-Jul-2013 24-Aug-2013 24-Sep-2013 24-Oct-2013 24-Nov-2013 24-Dec-2013 24-Jan-2014 24-Feb-2014 24-Mar-2014 24-Apr-2014 24-May-2014 24-Jun-2014 24-Jul-2014 24-Aug-2014 24-Sep-2014 24-Oct-2014 24-Nov-2014 24-Dec-2014 24-Jan-2015 24-Feb-2015 24-Mar-2015 24-Apr-2015 24-May-2015 24-Jun-2015 24-Jul-2015 24-Aug-2015 24-Sep-2015 24-Oct-2015 24-Nov-2015 24-Dec-2015 24-Jan-2016 24-Feb-2016 24-Mar-2016 24-Apr-2016 24-May-2016 24-Jun-2016 24-Jul-2016 24-Aug-2016 24-Sep-2016 24-Oct-2016 24-Nov-2016 24-Dec-2016 24-Jan-2017 24-Feb-2017 24-Mar-2017 24-Apr-2017 24-May-2017 24-Jun-2017 24-Jul-2017 24-Aug-2017 24-Sep-2017 24-Oct-2017 24-Nov-2017 24-Dec-2017 24-Jan-2018 24-Feb-2018 24-Mar-2018 24-Apr-2018 24-May-2018 24-Jun-2018 24-Jul-2018 24-Aug-2018 24-Sep-2018 24-Oct-2018 24-Nov-2018 24-Dec-2018 24-Jan-2019 24-Feb-2019 24-Mar-2019 24-Apr-2019 24-May-2019 24-Jun-2019 24-Jul-2019 24-Aug-2019 24-Sep-2019 24-Oct-2019 24-Nov-2019 24-Dec-2019 24-Jan-2020 24-Feb-2020 24-Mar-2020 24-Apr-2020 24-May-2020 24-Jun-2020 24-Jul-2020 24-Aug-2020 24-Sep-2020 24-Oct-2020 24-Nov-2020 24-Dec-2020 24-Jan-2021 24-Feb-2021 24-Mar-2021 24-Apr-2021 24-May-2021 24-Jun-2021 24-Jul-2021 24-Aug-2021 24-Sep-2021 24-Oct-2021 24-Nov-2021 24-Dec-2021 24-Jan-2022 24-Feb-2022 24-Mar-2022 24-Apr-2022 24-May-2022 24-Jun-2022 24-Jul-2022 24-Aug-2022 24-Sep-2022 24-Oct-2022 24-Nov-2022 24-Dec-2022 24-Jan-2023 24-Feb-2023 24-Mar-2023 24-Apr-2023 24-May-2023 24-Jun-2023 24-Jul-2023 24-Aug-2023 24-Sep-2023 24-Oct-2023 24-Nov-2023 24-Dec-2023 24-Jan-2024 24-Feb-2024 24-Mar-2024 24-Apr-2024 24-May-2024 24-Jun-2024 24-Jul-2024 24-Aug-2024 24-Sep-2024 24-Oct-2024 24-Nov-2024 24-Dec-2024 24-Jan-2025 24-Feb-2025 24-Mar-2025 24-Apr-2025 24-May-2025 24-Jun-2025 24-Jul-2025 24-Aug-2025 24-Sep-2025 24-Oct-2025 24-Nov-2025 24-Dec-2025 24-Jan-2026 24-Feb-2026 24-Mar-2026 24-Apr-2026 24-May-2026 24-Jun-2026 24-Jul-2026 24-Aug-2026 24-Sep-2026 24-Oct-2026 24-Nov-2026 24-Dec-2026 24-Jan-2027 24-Feb-2027 24-Mar-2027 24-Apr-2027 24-May-2027 24-Jun-2027 24-Jul-2027 24-Aug-2027 24-Sep-2027 24-Oct-2027 24-Nov-2027 24-Dec-2027 24-Jan-2028 24-Feb-2028 24-Mar-2028 24-Apr-2028 24-May-2028 24-Jun-2028 24-Jul-2028 24-Aug-2028 24-Sep-2028 24-Oct-2028 24-Nov-2028 24-Dec-2028 24-Jan-2029 24-Feb-2029 24-Mar-2029 24-Apr-2029 24-May-2029 24-Jun-2029 24-Jul-2029 24-Aug-2029 24-Sep-2029 24-Oct-2029 24-Nov-2029 24-Dec-2029 24-Jan-2030 24-Feb-2030 24-Mar-2030 24-Apr-2030 24-May-2030 24-Jun-2030 24-Jul-2030 24-Aug-2030 24-Sep-2030 24-Oct-2030 24-Nov-2030 24-Dec-2030 24-Jan-2031 24-Feb-2031 24-Mar-2031 24-Apr-2031 24-May-2031 24-Jun-2031 24-Jul-2031 24-Aug-2031 24-Sep-2031 24-Oct-2031 24-Nov-2031 24-Dec-2031 24-Jan-2032 24-Feb-2032 24-Mar-2032 24-Apr-2032 24-May-2032 24-Jun-2032 24-Jul-2032 24-Aug-2032 24-Sep-2032 24-Oct-2032 24-Nov-2032 24-Dec-2032 24-Jan-2033 24-Feb-2033 24-Mar-2033 24-Apr-2033 24-May-2033 24-Jun-2033 24-Jul-2033 24-Aug-2033 24-Sep-2033 24-Oct-2033 24-Nov-2033 24-Dec-2033 24-Jan-2034 24-Feb-2034 24-Mar-2034 24-Apr-2034 24-May-2034 24-Jun-2034 24-Jul-2034 24-Aug-2034 24-Sep-2034 24-Oct-2034 24-Nov-2034 24-Dec-2034 24-Jan-2035 24-Feb-2035 24-Mar-2035 24-Apr-2035 24-May-2035 24-Jun-2035 24-Jul-2035 24-Aug-2035 24-Sep-2035 24-Oct-2035 24-Nov-2035 24-Dec-2035 24-Jan-2036 24-Feb-2036 24-Mar-2036 24-Apr-2036 24-May-2036 24-Jun-2036 24-Jul-2036 24-Aug-2036 24-Sep-2036 24-Oct-2036 24-Nov-2036 24-Dec-2036 24-Jan-2037 24-Feb-2037 24-Mar-2037 24-Apr-2037 24-May-2037 24-Jun-2037 24-Jul-2037 24-Aug-2037 24-Sep-2037 24-Oct-2037 24-Nov-2037 24-Dec-2037 24-Jan-2038 24-Feb-2038 24-Mar-2038 24-Apr-2038 24-May-2038 24-Jun-2038 24-Jul-2038 24-Aug-2038 24-Sep-2038 24-Oct-2038 24-Nov-2038 24-Dec-2038 24-Jan-2039 24-Feb-2039 24-Mar-2039 24-Apr-2039 24-May-2039 24-Jun-2039 24-Jul-2039 24-Aug-2039 24-Sep-2039 24-Oct-2039 24-Nov-2039

rates = zerorates(SvenModel,maturities)

rates = 1×360

0.0083 0.0094 0.0105 0.0114 0.0124 0.0134 0.0143 0.0153 0.0162 0.0171 0.0179 0.0188 0.0196 0.0204 0.0212 0.0219 0.0226 0.0234 0.0241 0.0248 0.0255 0.0262 0.0268 0.0275 0.0281 0.0287 0.0293 0.0299 0.0304 0.0310 0.0316 0.0321 0.0326 0.0332 0.0336 0.0342 0.0346 0.0351 0.0356 0.0360 0.0365 0.0369 0.0373 0.0377 0.0382 0.0386 0.0389 0.0393 0.0397 0.0401

Plot the zero coupon rate.

plot(maturities,rates) xtickformat('yyyy') grid('on') xlabel('Time in Years') ylabel('Zero Coupon Rate')