Corporate Credit Risk

Simulate default credit risk, given a portfolio of assets, to determine how much might be lost

in a given time period due to credit defaults using the

creditDefaultCopula object. Simulate credit portfolio

value changes due to credit rating migrations of companies over some time

period using the creditMigrationCopula object. Analyze

the probability of a firm’s default using the Merton model and investigate

the concentration risk of your assets using concentration indices.

Additional tools to estimate default probabilities and transition

probabilities are in Financial Toolbox™ and additional classification models are in Statistics and Machine Learning Toolbox™.

Categories

- Simulate Default Credit Risk

Simulate default credit risk for a portfolio of credit instruments using copulas

- Simulate Credit Rating Migration Risk

Simulate credit portfolio value changes due to credit rating migrations using copulas

- Asymptotic Single Risk Factor Model Capital

Compute necessary capital using an asymptotic single risk factor (ASRF) model

- Default Probability Using Merton Model

Estimates the probability of default of a firm using the Merton option pricing formula

- Concentration Indices

Compute concentration measures for credit portfolios

- Credit Default Swaps

Bootstrap CDS probability curve, and determine CDS price and spread using Financial Toolbox

- Bootstrap Default Probabilities from Bonds

Bootstrap default probability curve from bond market prices using Financial Toolbox

- Estimate Transition Probabilities

Estimate change in credit quality, model transition probabilities from credit rating data using Financial Toolbox

- Determine Credit Quality Thresholds

Convert transition probabilities to credit quality thresholds and the opposite way using Financial Toolbox

Featured Examples

One-Factor Model Calibration

Demonstrates techniques to calibrate a one-factor model for estimating portfolio credit losses using the creditDefaultCopula or creditMigrationCopula classes.

Calculating Regulatory Capital with the ASRF Model

Calculate capital requirements and value-at-risk (VaR) for a credit sensitive portfolio of exposures using the asymptotic single risk factor (ASRF) model.

Credit Rating by Bagging Decision Trees

Build an automated credit rating tool.

Credit Rating by Ordinal Multinomial Regression

Use ordinal multinomial logistic regression to build a credit rating model that you can use in an automated credit rating process.

Compare Deep Learning Networks for Credit Default Prediction

Create, train, and compare three deep learning networks for predicting credit default probability.

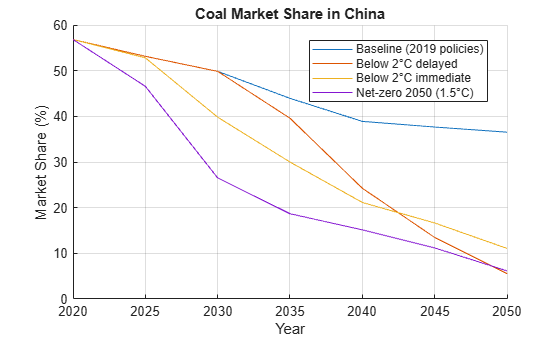

Measure Transition Risk for Loan Portfolios with Respect to Climate Scenarios

The effect of transition risk on portfolios of loans from two banks given three different climate scenarios. Potentially, climate change is a large structural change affecting the economy and the financial system. Clear physical risks are associated with climate change, including increases in the global average temperature and an increased frequency and severity of extreme weather events. These events could result in significant macroeconomic and financial system impacts. In addition to physical risk, another type of risk called transition risk arises from changes in policy and new technologies, such as the growth of renewable energy.