Vanilla

Vanilla instrument object

Description

Create and price a Vanilla instrument object for one or

more Vanilla instruments using this workflow:

Use

fininstrumentto create aVanillainstrument object for one or more Vanilla instruments.Use

finmodelto specify aBlackScholes,Bachelier,Heston,Bates,Merton,RoughBergomi,RoughHeston, orDupiremodel for theVanillainstrument object.Choose a pricing method.

When using a

BlackScholesmodel, usefinpricerto specify aFiniteDifference,BlackScholes,BjerksundStensland,RollGeskeWhaley,VannaVolga,AssetTree, orAssetMonteCarlopricing method for one or moreVanillainstruments.When using a

BlackScholesmodel, usefinpricerto specify anAssetReinforcementLearningpricing method for aVanillainstrument with anExerciseStyleof"American"or"Bermudan".When using a

Hestonmodel, usefinpricerto specify anAssetReinforcementLearningpricing method for aVanillainstrument with anExerciseStyleof"American"or"Bermudan".When using a

Heston,Bates, orMertonmodel, usefinpricerto specify aFiniteDifference,NumericalIntegration,FFT, orAssetMonteCarlopricing method for one or moreVanillainstruments.When using a

Dupiremodel, usefinpricerto specify aFiniteDifferencepricing method for one or moreVanillainstruments.When using a

Bacheliermodel, usefinpricerto specify anAssetMonteCarlopricing method for one or moreVanillainstruments.When using a

RoughBergomiorRoughHestonmodel, usefinpricerto specify aRoughVolMonteCarlopricing method for one or moreVanillainstruments.

For more information on this workflow, see Get Started with Workflows Using Object-Based Framework for Pricing Financial Instruments.

For more information on the available models and pricing methods for a

Vanilla instrument, see Choose Instruments, Models, and Pricers.

Creation

Syntax

Description

VanillaObj = fininstrument(InstrumentType,'Strike',strike_value,'ExerciseDate',exercise_date)Vanilla object for one or more Vanilla

instruments by specifying InstrumentType and sets the

properties for the

required name-value pair arguments Strike and

ExerciseDate. For more information on a

Vanilla instrument, see More About.

VanillaObj = fininstrument(___,Name,Value)VanillaObj =

fininstrument("Vanilla",'Strike',100,'ExerciseDate',datetime(2019,1,30),'OptionType',"put",'ExerciseStyle',"American",'Name',"vanilla_instrument")

creates a Vanilla put option with an American exercise.

You can specify multiple name-value pair arguments.

Input Arguments

Name-Value Arguments

Output Arguments

Properties

Object Functions

setExercisePolicy | Set exercise policy for FixedBondOption,

FloatBondOption, or Vanilla instrument |

Examples

This example shows the workflow to price a Vanilla instrument when you use a BlackScholes model and a BlackScholes pricing method.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",'ExerciseDate',datetime(2018,5,1),'Strike',29,'OptionType',"put",'ExerciseStyle',"european",'Name',"vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "put"

ExerciseStyle: "european"

ExerciseDate: 01-May-2018

Strike: 29

Name: "vanilla_option"

Create BlackScholes Model Object

Use finmodel to create a BlackScholes model object.

BlackScholesModel = finmodel("BlackScholes",'Volatility',0.25)

BlackScholesModel =

BlackScholes with properties:

Volatility: 0.2500

Correlation: 1

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,1,1); Maturity = datetime(2019,1,1); Rate = 0.05; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',1)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 1

Dates: 01-Jan-2019

Rates: 0.0500

Settle: 01-Jan-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create BlackScholes Pricer Object

Use finpricer to create a BlackScholes pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("analytic",'DiscountCurve',myRC,'Model',BlackScholesModel,'SpotPrice',30,'DividendValue',0.045)

outPricer =

BlackScholes with properties:

DiscountCurve: [1×1 ratecurve]

Model: [1×1 finmodel.BlackScholes]

SpotPrice: 30

DividendValue: 0.0450

DividendType: "continuous"

Price Vanilla Instrument

Use price to compute the price and sensitivities for the Vanilla instrument.

[Price, outPR] = price(outPricer,VanillaOpt,["all"])Price = 1.2046

outPR =

priceresult with properties:

Results: [1×7 table]

PricerData: []

outPR.Results

ans=1×7 table

Price Delta Gamma Lambda Vega Rho Theta

______ ________ ________ _______ ______ _______ _______

1.2046 -0.36943 0.086269 -9.3396 6.4702 -4.0959 -2.3107

This example shows the workflow to price multiple Vanilla instrument when you use a BlackScholes model and a BlackScholes pricing method.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object for three Vanilla instruments.

VanillaOpt = fininstrument("Vanilla",'ExerciseDate',datetime([2018,5,1 ; 2018,6,1 ; 2018,7,1]),'Strike',[29 ; 38 ; 70],'OptionType',"put",'ExerciseStyle',"european",'Name',"vanilla_option")

VanillaOpt=3×1 Vanilla array with properties:

OptionType

ExerciseStyle

ExerciseDate

Strike

Name

Create BlackScholes Model Object

Use finmodel to create a BlackScholes model object.

BlackScholesModel = finmodel("BlackScholes",'Volatility',0.25)

BlackScholesModel =

BlackScholes with properties:

Volatility: 0.2500

Correlation: 1

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,1,1); Maturity = datetime(2019,1,1); Rate = 0.05; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',1)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 1

Dates: 01-Jan-2019

Rates: 0.0500

Settle: 01-Jan-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create BlackScholes Pricer Object

Use finpricer to create a BlackScholes pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("analytic",'DiscountCurve',myRC,'Model',BlackScholesModel,'SpotPrice',30,'DividendValue',0.045)

outPricer =

BlackScholes with properties:

DiscountCurve: [1×1 ratecurve]

Model: [1×1 finmodel.BlackScholes]

SpotPrice: 30

DividendValue: 0.0450

DividendType: "continuous"

Price Vanilla Instruments

Use price to compute the prices and sensitivities for the Vanilla instruments.

[Price, outPR] = price(outPricer,VanillaOpt,["all"])Price = 3×1

1.2046

7.9479

38.9392

outPR=3×1 priceresult array with properties:

Results

PricerData

outPR.Results

ans=1×7 table

Price Delta Gamma Lambda Vega Rho Theta

______ ________ ________ _______ ______ _______ _______

1.2046 -0.36943 0.086269 -9.3396 6.4702 -4.0959 -2.3107

ans=1×7 table

Price Delta Gamma Lambda Vega Rho Theta

______ ________ ________ _______ ______ _______ _______

7.9479 -0.89786 0.031587 -3.4532 2.9612 -14.535 -0.3563

ans=1×7 table

Price Delta Gamma Lambda Vega Rho Theta

______ ________ __________ ________ __________ _______ ______

38.939 -0.97775 1.2279e-06 -0.77043 0.00013814 -34.136 2.0936

This example shows the workflow to price a Vanilla instrument when you use a BlackScholes model and an AssetTree pricing method using a Leisen-Reimer (LR) binomial tree.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",'ExerciseDate',datetime(2018,5,1),'Strike',29,'OptionType',"put",'ExerciseStyle',"european",'Name',"vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "put"

ExerciseStyle: "european"

ExerciseDate: 01-May-2018

Strike: 29

Name: "vanilla_option"

Create BlackScholes Model Object

Use finmodel to create a BlackScholes model object.

BlackScholesModel = finmodel("BlackScholes",'Volatility',0.25)

BlackScholesModel =

BlackScholes with properties:

Volatility: 0.2500

Correlation: 1

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,1,1); Maturity = datetime(2019,1,1); Rate = 0.05; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',1)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 1

Dates: 01-Jan-2019

Rates: 0.0500

Settle: 01-Jan-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create AssetTree Pricer Object

Use finpricer to create an AssetTree pricer object for a LR equity tree and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

NumPeriods = 15; LRPricer = finpricer("AssetTree",'DiscountCurve',myRC,'Model',BlackScholesModel,'SpotPrice',50,'PricingMethod',"LeisenReimer",'Maturity',datetime(2018,5,1),'NumPeriods',NumPeriods)

LRPricer =

LRTree with properties:

InversionMethod: PP1

Strike: 50

Tree: [1×1 struct]

NumPeriods: 15

Model: [1×1 finmodel.BlackScholes]

DiscountCurve: [1×1 ratecurve]

SpotPrice: 50

DividendType: "continuous"

DividendValue: 0

TreeDates: [09-Jan-2018 17-Jan-2018 25-Jan-2018 02-Feb-2018 10-Feb-2018 18-Feb-2018 26-Feb-2018 06-Mar-2018 14-Mar-2018 22-Mar-2018 30-Mar-2018 07-Apr-2018 15-Apr-2018 23-Apr-2018 01-May-2018]

LRPricer.Tree

ans = struct with fields:

Probs: [2×15 double]

ATree: {1×16 cell}

dObs: [01-Jan-2018 09-Jan-2018 17-Jan-2018 25-Jan-2018 02-Feb-2018 10-Feb-2018 18-Feb-2018 26-Feb-2018 06-Mar-2018 14-Mar-2018 22-Mar-2018 30-Mar-2018 07-Apr-2018 15-Apr-2018 23-Apr-2018 01-May-2018]

tObs: [0 0.0222 0.0444 0.0667 0.0889 0.1111 0.1333 0.1556 0.1778 0.2000 0.2222 0.2444 0.2667 0.2889 0.3111 0.3333]

Price Vanilla Instrument

Use price to compute the price and sensitivities for the Vanilla instrument.

[Price, outPR] = price(LRPricer,VanillaOpt,["all"])Price = 3.5022e-06

outPR =

priceresult with properties:

Results: [1×7 table]

PricerData: [1×1 struct]

outPR.Results

ans=1×7 table

Price Delta Gamma Vega Lambda Rho Theta

__________ ___________ __________ _________ _______ ___________ ___________

3.5022e-06 -1.9331e-06 1.1068e-06 0.0016243 -30.496 -3.6747e-05 -0.00060106

outPR.PricerData.PriceTree

ans = struct with fields:

PTree: {1×16 cell}

ExTree: {1×16 cell}

tObs: [0 0.0222 0.0444 0.0667 0.0889 0.1111 0.1333 0.1556 0.1778 0.2000 0.2222 0.2444 0.2667 0.2889 0.3111 0.3333]

dObs: [01-Jan-2018 09-Jan-2018 17-Jan-2018 25-Jan-2018 02-Feb-2018 10-Feb-2018 18-Feb-2018 26-Feb-2018 06-Mar-2018 14-Mar-2018 22-Mar-2018 30-Mar-2018 07-Apr-2018 15-Apr-2018 23-Apr-2018 01-May-2018]

Probs: [2×15 double]

outPR.PricerData.PriceTree.ExTree

ans=1×16 cell array

{[0]} {[0 0]} {[0 0 0]} {[0 0 0 0]} {[0 0 0 0 0]} {[0 0 0 0 0 0]} {[0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1]}

This example shows the workflow to price a Vanilla instrument when you use a BlackScholes model and an AssetTree pricing method using a Standard Trinomial (STT) tree.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",'ExerciseDate',datetime(2018,5,1),'Strike',29,'OptionType',"put",'ExerciseStyle',"european",'Name',"vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "put"

ExerciseStyle: "european"

ExerciseDate: 01-May-2018

Strike: 29

Name: "vanilla_option"

Create BlackScholes Model Object

Use finmodel to create a BlackScholes model object.

BlackScholesModel = finmodel("BlackScholes",'Volatility',0.25)

BlackScholesModel =

BlackScholes with properties:

Volatility: 0.2500

Correlation: 1

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,1,1); Maturity = datetime(2019,1,1); Rate = 0.05; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',1)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 1

Dates: 01-Jan-2019

Rates: 0.0500

Settle: 01-Jan-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create AssetTree Pricer Object

Use finpricer to create an AssetTree pricer object for a Standard Trinomial (STT) equity tree and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

NumPeriods = 15; STTPricer = finpricer("AssetTree",'DiscountCurve',myRC,'Model',BlackScholesModel,'SpotPrice',50,'PricingMethod',"StandardTrinomial",'Maturity',datetime(2018,5,1),'NumPeriods',NumPeriods)

STTPricer =

STTree with properties:

Tree: [1×1 struct]

NumPeriods: 15

Model: [1×1 finmodel.BlackScholes]

DiscountCurve: [1×1 ratecurve]

SpotPrice: 50

DividendType: "continuous"

DividendValue: 0

TreeDates: [09-Jan-2018 17-Jan-2018 25-Jan-2018 02-Feb-2018 10-Feb-2018 18-Feb-2018 26-Feb-2018 06-Mar-2018 14-Mar-2018 22-Mar-2018 30-Mar-2018 07-Apr-2018 15-Apr-2018 23-Apr-2018 01-May-2018]

STTPricer.Tree

ans = struct with fields:

ATree: {1×16 cell}

Probs: {[3×1 double] [3×3 double] [3×5 double] [3×7 double] [3×9 double] [3×11 double] [3×13 double] [3×15 double] [3×17 double] [3×19 double] [3×21 double] [3×23 double] [3×25 double] [3×27 double] [3×29 double]}

dObs: [01-Jan-2018 09-Jan-2018 17-Jan-2018 25-Jan-2018 02-Feb-2018 10-Feb-2018 18-Feb-2018 26-Feb-2018 06-Mar-2018 14-Mar-2018 22-Mar-2018 30-Mar-2018 07-Apr-2018 15-Apr-2018 23-Apr-2018 01-May-2018]

tObs: [0 0.0222 0.0444 0.0667 0.0889 0.1111 0.1333 0.1556 0.1778 0.2000 0.2222 0.2444 0.2667 0.2889 0.3111 0.3333]

Price Vanilla Instrument

Use price to compute the price and sensitivities for the Vanilla instrument.

[Price, outPR] = price(STTPricer,VanillaOpt,["all"])Price = 6.3773e-05

outPR =

priceresult with properties:

Results: [1×7 table]

PricerData: [1×1 struct]

outPR.Results

ans=1×7 table

Price Delta Gamma Vega Lambda Rho Theta

__________ ___________ __________ _________ _______ ___________ _________

6.3773e-05 -9.1432e-06 1.2388e-06 0.0034421 -21.514 -0.00064994 -0.001188

outPR.PricerData.PriceTree

ans = struct with fields:

PTree: {1×16 cell}

ExTree: {1×16 cell}

tObs: [0 0.0222 0.0444 0.0667 0.0889 0.1111 0.1333 0.1556 0.1778 0.2000 0.2222 0.2444 0.2667 0.2889 0.3111 0.3333]

dObs: [01-Jan-2018 09-Jan-2018 17-Jan-2018 25-Jan-2018 02-Feb-2018 10-Feb-2018 18-Feb-2018 26-Feb-2018 06-Mar-2018 14-Mar-2018 22-Mar-2018 30-Mar-2018 07-Apr-2018 15-Apr-2018 23-Apr-2018 01-May-2018]

Probs: {[3×1 double] [3×3 double] [3×5 double] [3×7 double] [3×9 double] [3×11 double] [3×13 double] [3×15 double] [3×17 double] [3×19 double] [3×21 double] [3×23 double] [3×25 double] [3×27 double] [3×29 double]}

outPR.PricerData.PriceTree.ExTree

ans=1×16 cell array

{[0]} {[0 0 0]} {[0 0 0 0 0]} {[0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0]} {[0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 1 1 1 1 1 1 1]}

This example shows the workflow to price an American option for a Vanilla instrument when you use a BlackScholes model and a RollGeskeWhaley pricing method.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",'Strike',105,'ExerciseDate',datetime(2022,9,15),'OptionType',"call",'ExerciseStyle',"american",'Name',"vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "call"

ExerciseStyle: "american"

ExerciseDate: 15-Sep-2022

Strike: 105

Name: "vanilla_option"

Create BlackScholes Model Object

Use finmodel to create a BlackScholes model object.

BlackScholesModel = finmodel("BlackScholes","Volatility",0.2)

BlackScholesModel =

BlackScholes with properties:

Volatility: 0.2000

Correlation: 1

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,9,15); Maturity = datetime(2023,9,15); Rate = 0.035; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',12)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 12

Dates: 15-Sep-2023

Rates: 0.0350

Settle: 15-Sep-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create RollGeskeWhaley Pricer Object

Use finpricer to create a RollGeskeWhaley pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("analytic",'Model',BlackScholesModel,'DiscountCurve',myRC,'SpotPrice',100,'DividendValue',timetable(datetime(2021,6,15),0.25),'PricingMethod',"RollGeskeWhaley")

outPricer =

RollGeskeWhaley with properties:

DiscountCurve: [1×1 ratecurve]

Model: [1×1 finmodel.BlackScholes]

SpotPrice: 100

DividendValue: [1×1 timetable]

DividendType: "cash"

Price Vanilla Instrument

Use price to compute the price and sensitivities for the Vanilla instrument.

[Price, outPR] = price(outPricer,VanillaOpt,["all"])Price = 19.9066

outPR =

priceresult with properties:

Results: [1×7 table]

PricerData: []

outPR.Results

ans=1×7 table

Price Delta Gamma Lambda Vega Theta Rho

______ _______ _________ ______ ______ _______ ______

19.907 0.66568 0.0090971 3.344 72.804 -3.4537 186.68

This example shows the workflow to price a Vanilla instrument for foreign exchange (FX) when you use a BlackScholes model and a BlackScholes pricing method. Assume that the current exchange rate is $0.52 and has a volatility of 12% per annum. The annualized continuously compounded foreign risk-free rate is 8% per annum.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",'ExerciseDate',datetime(2022,9,15),'Strike',.50,'OptionType',"put",'ExerciseStyle',"european",'Name',"vanilla_fx_option")

VanillaOpt =

Vanilla with properties:

OptionType: "put"

ExerciseStyle: "european"

ExerciseDate: 15-Sep-2022

Strike: 0.5000

Name: "vanilla_fx_option"

Create BlackScholes Model Object

Use finmodel to create a BlackScholes model object.

Sigma = .12; BlackScholesModel = finmodel("BlackScholes","Volatility",Sigma)

BlackScholesModel =

BlackScholes with properties:

Volatility: 0.1200

Correlation: 1

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,9,15); Maturity = datetime(2023,9,15); Rate = 0.035; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',12)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 12

Dates: 15-Sep-2023

Rates: 0.0350

Settle: 15-Sep-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create BlackScholes Pricer Object

Use finpricer to create a BlackScholes pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument. When pricing currencies using a Vanilla instrument, the DividendType must be 'continuous' and DividendValue is the annualized risk-free interest rate in the foreign country.

ForeignRate = 0.08; outPricer = finpricer("analytic",'DiscountCurve',myRC,'Model',BlackScholesModel,'SpotPrice',.52,'DividendType',"continuous",'DividendValue',ForeignRate)

outPricer =

BlackScholes with properties:

DiscountCurve: [1×1 ratecurve]

Model: [1×1 finmodel.BlackScholes]

SpotPrice: 0.5200

DividendValue: 0.0800

DividendType: "continuous"

Price Vanilla FX Instrument

Use price to compute the price and sensitivities for the Vanilla FX instrument.

[Price, outPR] = price(outPricer,VanillaOpt,["all"])Price = 0.0738

outPR =

priceresult with properties:

Results: [1×7 table]

PricerData: []

outPR.Results

ans=1×7 table

Price Delta Gamma Lambda Vega Rho Theta

________ ________ ______ _______ _______ _______ _________

0.073778 -0.49349 2.0818 -4.7899 0.27021 -1.3216 -0.013019

This example shows the workflow to price an American option for a Vanilla instrument when you use a BlackScholes model and an AssetMonteCarlo pricing method.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",'Strike',105,'ExerciseDate',datetime(2022,9,15),'OptionType',"call",'ExerciseStyle',"american",'Name',"vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "call"

ExerciseStyle: "american"

ExerciseDate: 15-Sep-2022

Strike: 105

Name: "vanilla_option"

Create BlackScholes Model Object

Use finmodel to create a BlackScholes model object.

BlackScholesModel = finmodel("BlackScholes","Volatility",0.2)

BlackScholesModel =

BlackScholes with properties:

Volatility: 0.2000

Correlation: 1

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,9,15); Maturity = datetime(2023,9,15); Rate = 0.035; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',12)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 12

Dates: 15-Sep-2023

Rates: 0.0350

Settle: 15-Sep-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create AssetMonteCarlo Pricer Object

Use finpricer to create an AssetMonteCarlo pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("AssetMonteCarlo",'DiscountCurve',myRC,"Model",BlackScholesModel,'SpotPrice',150,'simulationDates',datetime(2022,9,15))

outPricer =

GBMMonteCarlo with properties:

DiscountCurve: [1×1 ratecurve]

SpotPrice: 150

SimulationDates: 15-Sep-2022

NumTrials: 1000

RandomNumbers: []

Model: [1×1 finmodel.BlackScholes]

DividendType: "continuous"

DividendValue: 0

MonteCarloMethod: "standard"

BrownianMotionMethod: "standard"

Price Vanilla Instrument

Use price to compute the price and sensitivities for the Vanilla instrument.

[Price, outPR] = price(outPricer,VanillaOpt,["all"])Price = 61.2010

outPR =

priceresult with properties:

Results: [1×7 table]

PricerData: [1×1 struct]

outPR.Results

ans=1×7 table

Price Delta Gamma Lambda Rho Theta Vega

______ _______ _________ ______ ______ _______ ______

61.201 0.93074 0.0027813 2.2812 313.95 -3.7909 41.626

This example shows the workflow to price an American option for a Vanilla instrument when you use a BlackScholes model and an AssetMonteCarlo pricing method with quasi-Monte Carlo simulation.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",'Strike',105,'ExerciseDate',datetime(2022,9,15),'OptionType',"call",'ExerciseStyle',"american",'Name',"vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "call"

ExerciseStyle: "american"

ExerciseDate: 15-Sep-2022

Strike: 105

Name: "vanilla_option"

Create BlackScholes Model Object

Use finmodel to create a BlackScholes model object.

BlackScholesModel = finmodel("BlackScholes","Volatility",0.2)

BlackScholesModel =

BlackScholes with properties:

Volatility: 0.2000

Correlation: 1

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,9,15); Maturity = datetime(2023,9,15); Rate = 0.035; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',12)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 12

Dates: 15-Sep-2023

Rates: 0.0350

Settle: 15-Sep-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create AssetMonteCarlo Pricer Object

Use finpricer to create an AssetMonteCarlo pricer object and use the ratecurve object for the 'DiscountCurve' name-value argument and the name-value arguments for MonteCarloMethod and BrownianMotionMethod.

outPricer = finpricer("AssetMonteCarlo",'DiscountCurve',myRC,"Model",BlackScholesModel,'SpotPrice',150,'simulationDates',datetime(2022,9,15),'NumTrials',1e3, ... 'MonteCarloMethod',"quasi",'BrownianMotionMethod',"brownian-bridge")

outPricer =

GBMMonteCarlo with properties:

DiscountCurve: [1×1 ratecurve]

SpotPrice: 150

SimulationDates: 15-Sep-2022

NumTrials: 1000

RandomNumbers: []

Model: [1×1 finmodel.BlackScholes]

DividendType: "continuous"

DividendValue: 0

MonteCarloMethod: "quasi"

BrownianMotionMethod: "brownian-bridge"

Price Vanilla Instrument

Use price to compute the price and sensitivities for the Vanilla instrument.

[Price, outPR] = price(outPricer,VanillaOpt,"all")Price = 60.7272

outPR =

priceresult with properties:

Results: [1×7 table]

PricerData: [1×1 struct]

outPR.Results

ans=1×7 table

Price Delta Gamma Lambda Rho Theta Vega

______ _______ _________ ______ ______ _______ ______

60.727 0.92248 0.0024038 2.2786 310.66 -3.7073 39.466

This example shows the workflow to price an American option for a Vanilla instrument when you use a Heston model and an AssetMonteCarlo pricing method.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",'Strike',105,'ExerciseDate',datetime(2022,9,15),'OptionType',"call",'ExerciseStyle',"american",'Name',"vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "call"

ExerciseStyle: "american"

ExerciseDate: 15-Sep-2022

Strike: 105

Name: "vanilla_option"

Create Heston Model Object

Use finmodel to create a Heston model object.

HestonModel = finmodel("Heston",'V0',0.032,'ThetaV',0.07,'Kappa',0.003,'SigmaV',0.02,'RhoSV',0.09)

HestonModel =

Heston with properties:

V0: 0.0320

ThetaV: 0.0700

Kappa: 0.0030

SigmaV: 0.0200

RhoSV: 0.0900

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,9,15); Maturity = datetime(2023,9,15); Rate = 0.035; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',12)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 12

Dates: 15-Sep-2023

Rates: 0.0350

Settle: 15-Sep-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create AssetMonteCarlo Pricer Object

Use finpricer to create an AssetMonteCarlo pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("AssetMonteCarlo",'DiscountCurve',myRC,"Model",HestonModel,'SpotPrice',150,'simulationDates',datetime(2022,9,15))

outPricer =

HestonMonteCarlo with properties:

DiscountCurve: [1×1 ratecurve]

SpotPrice: 150

SimulationDates: 15-Sep-2022

NumTrials: 1000

RandomNumbers: []

Model: [1×1 finmodel.Heston]

DividendType: "continuous"

DividendValue: 0

MonteCarloMethod: "standard"

BrownianMotionMethod: "standard"

Price Vanilla Instrument

Use price to compute the price and sensitivities for the Vanilla instrument.

[Price, outPR] = price(outPricer,VanillaOpt,["all"])Price = 60.5637

outPR =

priceresult with properties:

Results: [1×8 table]

PricerData: [1×1 struct]

outPR.Results

ans=1×8 table

Price Delta Gamma Lambda Rho Theta Vega VegaLT

______ _______ _________ ______ ______ _______ ______ _______

60.564 0.94774 0.0011954 2.3473 326.36 -3.7126 35.272 0.31155

This example shows the workflow to price a Bermudan option for a Vanilla instrument when you use a BlackScholes model and a FiniteDifference pricing method.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",'Strike',[110,120],'ExerciseDate',[datetime(2022,9,15) , datetime(2023,9,15)],'OptionType',"call",'ExerciseStyle',"Bermudan",'Name',"vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "call"

ExerciseStyle: "bermudan"

ExerciseDate: [15-Sep-2022 15-Sep-2023]

Strike: [110 120]

Name: "vanilla_option"

Create BlackScholes Model Object

Use finmodel to create a BlackScholes model object.

BlackScholesModel = finmodel("BlackScholes","Volatility",0.2)

BlackScholesModel =

BlackScholes with properties:

Volatility: 0.2000

Correlation: 1

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,9,15); Maturity = datetime(2023,9,15); Rate = 0.035; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',12)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 12

Dates: 15-Sep-2023

Rates: 0.0350

Settle: 15-Sep-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create FiniteDifference Pricer Object

Use finpricer to create a FiniteDifference pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("FiniteDifference",'Model',BlackScholesModel,'DiscountCurve',myRC,'SpotPrice',100)

outPricer =

FiniteDifference with properties:

DiscountCurve: [1×1 ratecurve]

Model: [1×1 finmodel.BlackScholes]

SpotPrice: 100

GridProperties: [1×1 struct]

DividendType: "continuous"

DividendValue: 0

Price Vanilla Instrument

Use price to compute the price and sensitivities for the Vanilla instrument.

[Price, outPR] = price(outPricer,VanillaOpt,["all"])Price = 18.6797

outPR =

priceresult with properties:

Results: [1×7 table]

PricerData: [1×1 struct]

outPR.Results

ans=1×7 table

Price Delta Gamma Lambda Theta Rho Vega

_____ _______ _________ ______ _______ ______ ______

18.68 0.62163 0.0091406 3.3278 -3.3154 184.31 83.162

This example shows the workflow to price a Vanilla instrument when you use a Heston model and various pricing methods.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

Settle = datetime(2017,6,29); Maturity = datemnth(Settle,6); Strike = 80; VanillaOpt = fininstrument('Vanilla','ExerciseDate',Maturity,'Strike',Strike,'Name',"vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "call"

ExerciseStyle: "european"

ExerciseDate: 29-Dec-2017

Strike: 80

Name: "vanilla_option"

Create Heston Model Object

Use finmodel to create a Heston model object.

V0 = 0.04; ThetaV = 0.05; Kappa = 1.0; SigmaV = 0.2; RhoSV = -0.7; HestonModel = finmodel("Heston",'V0',V0,'ThetaV',ThetaV,'Kappa',Kappa,'SigmaV',SigmaV,'RhoSV',RhoSV)

HestonModel =

Heston with properties:

V0: 0.0400

ThetaV: 0.0500

Kappa: 1

SigmaV: 0.2000

RhoSV: -0.7000

Create ratecurve object

Create a ratecurve object using ratecurve.

Rate = 0.03;

ZeroCurve = ratecurve('zero',Settle,Maturity,Rate);Create NumericalIntegration, FFT, and FiniteDifference Pricer Objects

Use finpricer to create a NumericalIntegration, FFT, and FiniteDifference pricer objects and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

SpotPrice = 80; Strike = 80; DividendYield = 0.02; NIPricer = finpricer("NumericalIntegration",'Model', HestonModel,'SpotPrice',SpotPrice,'DiscountCurve',ZeroCurve,'DividendValue',DividendYield)

NIPricer =

NumericalIntegration with properties:

Model: [1×1 finmodel.Heston]

DiscountCurve: [1×1 ratecurve]

SpotPrice: 80

DividendType: "continuous"

DividendValue: 0.0200

AbsTol: 1.0000e-10

RelTol: 1.0000e-10

IntegrationRange: [1.0000e-09 Inf]

CharacteristicFcn: @characteristicFcnHeston

Framework: "heston1993"

VolRiskPremium: 0

LittleTrap: 1

FFTPricer = finpricer("FFT",'Model',HestonModel, ... 'SpotPrice',SpotPrice,'DiscountCurve',ZeroCurve, ... 'DividendValue',DividendYield,'NumFFT',8192)

FFTPricer =

FFT with properties:

Model: [1×1 finmodel.Heston]

DiscountCurve: [1×1 ratecurve]

SpotPrice: 80

DividendType: "continuous"

DividendValue: 0.0200

NumFFT: 8192

CharacteristicFcnStep: 0.0100

LogStrikeStep: 0.0767

CharacteristicFcn: @characteristicFcnHeston

DampingFactor: 1.5000

Quadrature: "simpson"

VolRiskPremium: 0

LittleTrap: 1

FDPricer = finpricer("FiniteDifference",'Model',HestonModel,'SpotPrice',SpotPrice,'DiscountCurve',ZeroCurve,'DividendValue',DividendYield)

FDPricer =

FiniteDifference with properties:

DiscountCurve: [1×1 ratecurve]

Model: [1×1 finmodel.Heston]

SpotPrice: 80

GridProperties: [1×1 struct]

DividendType: "continuous"

DividendValue: 0.0200

Price Vanilla Instrument

Use the following sensitivities when pricing the Vanilla instrument.

InpSensitivity = ["delta", "gamma", "theta", "rho", "vega", "vegalt"];

Use price to compute the price and sensitivities for the Vanilla instrument that uses the NumericalIntegration pricer.

[PriceNI, outPR_NI] = price(NIPricer,VanillaOpt,InpSensitivity)

PriceNI = 4.7007

outPR_NI =

priceresult with properties:

Results: [1×7 table]

PricerData: []

Use price to compute the price and sensitivities for the Vanilla instrument that uses the FFT pricer.

[PriceFFT, outPR_FFT] = price(FFTPricer,VanillaOpt,InpSensitivity)

PriceFFT = 4.7007

outPR_FFT =

priceresult with properties:

Results: [1×7 table]

PricerData: []

Use price to compute the price and sensitivities for the Vanilla instrument that uses the FiniteDifference pricer.

[PriceFD, outPR_FD] = price(FDPricer,VanillaOpt,InpSensitivity)

PriceFD = 4.7003

outPR_FD =

priceresult with properties:

Results: [1×7 table]

PricerData: [1×1 struct]

Aggregate the price results.

[outPR_NI.Results;outPR_FFT.Results;outPR_FD.Results]

ans=3×7 table

Price Delta Gamma Theta Rho Vega VegaLT

______ _______ ________ _______ ______ ______ ______

4.7007 0.57747 0.03392 -4.8474 20.805 17.028 5.2394

4.7007 0.57747 0.03392 -4.8474 20.805 17.028 5.2394

4.7003 0.57722 0.035254 -4.8483 20.801 17.046 5.2422

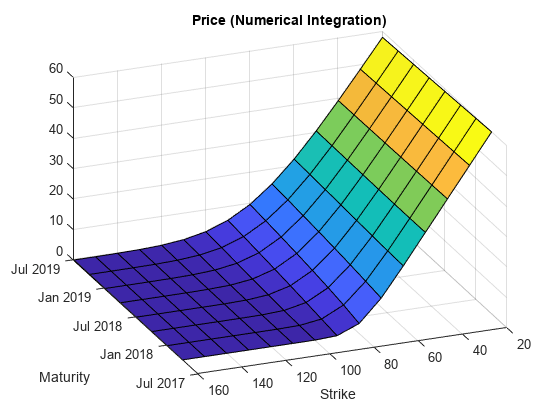

Compute Option Price Surfaces

Use the price function for the NumericalIntegration pricer and the price function for the FFT pricer to compute the prices for a range of Vanilla instruments.

Maturities = datemnth(Settle,(3:3:24)'); NumMaturities = length(Maturities); Strikes = (20:10:160)'; NumStrikes = length(Strikes); [Maturities_Full,Strikes_Full] = meshgrid(Maturities,Strikes); NumInst = numel(Strikes_Full); VanillaOptions(NumInst, 1) = fininstrument("vanilla", ... "ExerciseDate", Maturities_Full(1), "Strike", Strikes_Full(1)); for instidx=1:NumInst VanillaOptions(instidx) = fininstrument("vanilla", ... "ExerciseDate", Maturities_Full(instidx), "Strike", Strikes_Full(instidx)); end Prices_NI = price(NIPricer, VanillaOptions); Prices_FFT = price(FFTPricer, VanillaOptions); figure; surf(Maturities_Full,Strikes_Full,reshape(Prices_NI,[NumStrikes,NumMaturities])); title('Price (Numerical Integration)'); view(-112,34); xlabel('Maturity') ylabel('Strike')

figure; surf(Maturities_Full,Strikes_Full,reshape(Prices_FFT,[NumStrikes,NumMaturities])); title('Price (FFT)'); view(-112,34); xlabel('Maturity') ylabel('Strike')

Since R2024a

This example shows the workflow to price a Vanilla instrument when you use a RoughBergomi model and a RoughVolMonteCarlo pricing method.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",'ExerciseDate',datetime(2019,1,30),'Strike',105,'ExerciseStyle',"european",'Name',"vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "call"

ExerciseStyle: "european"

ExerciseDate: 30-Jan-2019

Strike: 105

Name: "vanilla_option"

Create RoughBergomi Model Object

Use finmodel to create a RoughBergomi model object.

RoughBergomiModel = finmodel("RoughBergomi",Alpha=-0.032,Xi=0.1,Eta=0.003,RhoSV=0.9)RoughBergomiModel =

RoughBergomi with properties:

Alpha: -0.0320

Xi: 0.1000

Eta: 0.0030

RhoSV: 0.9000

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,9,15); Maturity = datetime(2023,9,15); Rate = 0.035; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',12)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 12

Dates: 15-Sep-2023

Rates: 0.0350

Settle: 15-Sep-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create RoughVolMonteCarlo Pricer Object

Use finpricer to create an RoughVolMonteCarlo pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

outPricer = finpricer("RoughVolMonteCarlo",DiscountCurve=myRC,Model=RoughBergomiModel,SpotPrice=100,SimulationDates=datetime(2019,1,30))outPricer =

RoughBergomiMonteCarlo with properties:

DiscountCurve: [1×1 ratecurve]

SpotPrice: 100

SimulationDates: 30-Jan-2019

NumTrials: 1000

RandomNumbers: []

Model: [1×1 finmodel.RoughBergomi]

DividendType: "continuous"

DividendValue: 0

MonteCarloMethod: "standard"

BrownianMotionMethod: "standard"

Price Vanilla Instrument

Use price to compute the price and sensitivities for the Vanilla instrument.

[Price, outPR] = price(outPricer,VanillaOpt,"all")Price = 7.7862

outPR =

priceresult with properties:

Results: [1×7 table]

PricerData: [1×1 struct]

outPR.Results

ans=1×7 table

Price Delta Gamma Lambda Rho Theta Vega

______ _______ ________ ______ ______ ______ ______

7.7862 0.50369 0.012632 6.469 15.947 1.0273 30.741

Since R2024b

This example shows the workflow to price a Vanilla instrument when you use a RoughHeston model and a RoughVolMonteCarlo pricing method.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",'ExerciseDate',datetime(2019,1,30),'Strike',105,'ExerciseStyle',"european",'Name',"vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "call"

ExerciseStyle: "european"

ExerciseDate: 30-Jan-2019

Strike: 105

Name: "vanilla_option"

Create RoughHeston Model Object

Use finmodel to create a RoughHeston model object.

RoughBergomiModel = finmodel("RoughHeston",V0=0.4,ThetaV=0.3,Kappa=0.2,SigmaV=0.1,Alpha=-0.02,RhoSV=0.3)RoughBergomiModel =

RoughHeston with properties:

Alpha: -0.0200

V0: 0.4000

ThetaV: 0.3000

Kappa: 0.2000

SigmaV: 0.1000

RhoSV: 0.3000

Create ratecurve Object

Create a flat ratecurve object using ratecurve.

Settle = datetime(2018,9,15); Maturity = datetime(2023,9,15); Rate = 0.035; myRC = ratecurve('zero',Settle,Maturity,Rate,'Basis',12)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 12

Dates: 15-Sep-2023

Rates: 0.0350

Settle: 15-Sep-2018

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create RoughVolMonteCarlo Pricer Object

Use finpricer to create an RoughVolMonteCarlo pricer object and use the ratecurve object for the 'DiscountCurve' name-value argument.

outPricer = finpricer("RoughVolMonteCarlo",DiscountCurve=myRC,Model=RoughBergomiModel,SpotPrice=100,SimulationDates=datetime(2019,1,30))outPricer =

RoughHestonMonteCarlo with properties:

DiscountCurve: [1×1 ratecurve]

SpotPrice: 100

SimulationDates: 30-Jan-2019

NumTrials: 1000

RandomNumbers: []

Model: [1×1 finmodel.RoughHeston]

DividendType: "continuous"

DividendValue: 0

MonteCarloMethod: "standard"

BrownianMotionMethod: "standard"

Price Vanilla Instrument

Use price to compute the price and sensitivities for the Vanilla instrument.

[Price, outPR] = price(outPricer,VanillaOpt,"all")Price = 13.9392

outPR =

priceresult with properties:

Results: [1×8 table]

PricerData: [1×1 struct]

outPR.Results

ans=1×8 table

Price Delta Gamma Lambda Rho Theta Vega VegaLT

______ _______ ________ ______ ______ _______ ______ ______

13.939 0.54193 0.011253 3.8878 15.143 -22.098 24.539 0

Since R2026a

This example shows the workflow to price a Vanilla instrument with an "American" ExerciseStyle when using a BlackScholes model and an AssetReinforcementLearning pricing method. Note, to use this functionality, you must have Reinforcement Learning Toolbox™ installed.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",ExerciseDate=datetime(2021,8,15),Strike=110,OptionType="put",ExerciseStyle="american",Name="vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "put"

ExerciseStyle: "american"

ExerciseDate: 15-Aug-2021

Strike: 110

Name: "vanilla_option"

Create BlackScholes Model Object

Use finmodel to create a BlackScholes model object.

BSModel = finmodel("BlackScholes",Volatility=0.2)BSModel =

BlackScholes with properties:

Volatility: 0.2000

Correlation: 1

Create ratecurve Object

Create a ratecurve object using ratecurve.

Settle = datetime(2019,1,1); Type = 'zero'; ZeroTimes = [calmonths(6) calyears([1 2 3 4 5 7 10 20 30])]'; ZeroRates = [0.0052 0.0055 0.0061 0.0073 0.0094 0.0119 0.0168 0.0222 0.0293 0.0307]'; ZeroDates = Settle + ZeroTimes; myRC = ratecurve('zero',Settle,ZeroDates,ZeroRates)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 0

Dates: [10×1 datetime]

Rates: [10×1 double]

Settle: 01-Jan-2019

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create AssetReinforcementLearning Pricer Object

Use finpricer to create an AssetReinforcementLearning pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

SpotPrice = 100;

SimDates = [Settle+days(1):days(2):Settle+years(2)];

outPricer = finpricer("AssetReinforcementLearning",DiscountCurve=myRC,Model=BSModel,SpotPrice=SpotPrice,SimulationDates=SimDates)outPricer =

AssetReinforcementLearning with properties:

DiscountCurve: [1×1 ratecurve]

SpotPrice: 100

SimulationDates: [02-Jan-2019 04-Jan-2019 06-Jan-2019 08-Jan-2019 10-Jan-2019 12-Jan-2019 14-Jan-2019 16-Jan-2019 18-Jan-2019 20-Jan-2019 22-Jan-2019 24-Jan-2019 26-Jan-2019 28-Jan-2019 … ] (1×365 datetime)

NumTrials: 1000

Model: [1×1 finmodel.BlackScholes]

DividendType: "continuous"

DividendValue: 0

Price Vanilla Instrument

Use price to compute the price for the Vanilla instrument.

[Price,priceResultData] = price(outPricer,VanillaOpt)

Price = 16.4847

priceResultData =

priceresult with properties:

Results: [1×1 table]

PricerData: [1×1 struct]

priceResultData.PricerData

ans = struct with fields:

SimulationTimes: [366×1 timetable]

Paths: [366×1×1000 double]

TrainingStats: [1×1 rl.train.result.rlTrainingResult]

Agent: [1×1 rl.agent.rlLSPIAmericanOptionAgent]

Since R2026a

This example shows the workflow to price a Vanilla instrument with an "Bermudan" ExerciseStyle when using a BlackScholes model and an AssetReinforcementLearning pricing method. Note, to use this functionality, you must have Reinforcement Learning Toolbox™ installed.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",ExerciseDate=[datetime(2019,1,16),datetime(2019,1,26)],Strike=110,OptionType="put",ExerciseStyle="bermudan",Name="vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "put"

ExerciseStyle: "bermudan"

ExerciseDate: [16-Jan-2019 26-Jan-2019]

Strike: [110 110]

Name: "vanilla_option"

Create BlackScholes Model Object

Use finmodel to create a BlackScholes model object.

BSModel = finmodel("BlackScholes",Volatility=0.2)BSModel =

BlackScholes with properties:

Volatility: 0.2000

Correlation: 1

Create ratecurve Object

Create a ratecurve object using ratecurve.

Settle = datetime(2019,1,1); Type = 'zero'; ZeroTimes = [calmonths(6) calyears([1 2 3 4 5 7 10 20 30])]'; ZeroRates = [0.0052 0.0055 0.0061 0.0073 0.0094 0.0119 0.0168 0.0222 0.0293 0.0307]'; ZeroDates = Settle + ZeroTimes; myRC = ratecurve('zero',Settle,ZeroDates,ZeroRates)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 0

Dates: [10×1 datetime]

Rates: [10×1 double]

Settle: 01-Jan-2019

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create AssetReinforcementLearning Pricer Object

Use finpricer to create an AssetReinforcementLearning pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

SpotPrice = 100;

SimDates = [Settle+days(1):days(2):Settle+calmonths(1)];

outPricer = finpricer("AssetReinforcementLearning",DiscountCurve=myRC,Model=BSModel,SpotPrice=SpotPrice,SimulationDates=SimDates)outPricer =

AssetReinforcementLearning with properties:

DiscountCurve: [1×1 ratecurve]

SpotPrice: 100

SimulationDates: [02-Jan-2019 04-Jan-2019 06-Jan-2019 08-Jan-2019 10-Jan-2019 12-Jan-2019 14-Jan-2019 16-Jan-2019 18-Jan-2019 20-Jan-2019 22-Jan-2019 24-Jan-2019 26-Jan-2019 28-Jan-2019 … ] (1×16 datetime)

NumTrials: 1000

Model: [1×1 finmodel.BlackScholes]

DividendType: "continuous"

DividendValue: 0

Price Vanilla Instrument

Use price to compute the price for the Vanilla instrument.

[Price,priceResultData] = price(outPricer,VanillaOpt)

Price = 9.9905

priceResultData =

priceresult with properties:

Results: [1×1 table]

PricerData: [1×1 struct]

priceResultData.PricerData

ans = struct with fields:

SimulationTimes: [17×1 timetable]

Paths: [17×1×1000 double]

TrainingStats: [1×1 rl.train.result.rlTrainingResult]

Agent: [1×1 rl.agent.rlLSPIAmericanOptionAgent]

Since R2026a

This example shows the workflow to price a Vanilla instrument with an "American" ExerciseStyle when using a Heston model and an AssetReinforcementLearning pricing method. Note, to use this functionality, you must have Reinforcement Learning Toolbox™ installed.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",ExerciseDate=datetime(2021,8,15),Strike=110,OptionType="put",ExerciseStyle="american",Name="vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "put"

ExerciseStyle: "american"

ExerciseDate: 15-Aug-2021

Strike: 110

Name: "vanilla_option"

Create Heston Model Object

Use finmodel to create a Heston model object.

HestonModel = finmodel("Heston",V0=0.032,ThetaV=0.1,Kappa=0.003,SigmaV=0.08,RhoSV=0.9)HestonModel =

Heston with properties:

V0: 0.0320

ThetaV: 0.1000

Kappa: 0.0030

SigmaV: 0.0800

RhoSV: 0.9000

Create ratecurve Object

Create a ratecurve object using ratecurve.

Settle = datetime(2019,1,1); Type = 'zero'; ZeroTimes = [calmonths(6) calyears([1 2 3 4 5 7 10 20 30])]'; ZeroRates = [0.0052 0.0055 0.0061 0.0073 0.0094 0.0119 0.0168 0.0222 0.0293 0.0307]'; ZeroDates = Settle + ZeroTimes; myRC = ratecurve('zero',Settle,ZeroDates,ZeroRates)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 0

Dates: [10×1 datetime]

Rates: [10×1 double]

Settle: 01-Jan-2019

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create AssetReinforcementLearning Pricer Object

Use finpricer to create an AssetReinforcementLearning pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

SpotPrice = 100;

SimDates = [Settle+days(1):days(2):Settle+years(2)];

outPricer = finpricer("AssetReinforcementLearning",DiscountCurve=myRC,Model=HestonModel,SpotPrice=SpotPrice,SimulationDates=SimDates)outPricer =

AssetReinforcementLearning with properties:

DiscountCurve: [1×1 ratecurve]

SpotPrice: 100

SimulationDates: [02-Jan-2019 04-Jan-2019 06-Jan-2019 08-Jan-2019 10-Jan-2019 12-Jan-2019 14-Jan-2019 16-Jan-2019 18-Jan-2019 20-Jan-2019 22-Jan-2019 24-Jan-2019 26-Jan-2019 28-Jan-2019 … ] (1×365 datetime)

NumTrials: 1000

Model: [1×1 finmodel.Heston]

DividendType: "continuous"

DividendValue: 0

Price Vanilla Instrument

Use price to compute the price for the Vanilla instrument.

[Price,priceResultData] = price(outPricer,VanillaOpt)

Price = 15.5194

priceResultData =

priceresult with properties:

Results: [1×1 table]

PricerData: [1×1 struct]

priceResultData.PricerData

ans = struct with fields:

SimulationTimes: [366×1 timetable]

Paths: [366×2×1000 double]

TrainingStats: [1×1 rl.train.result.rlTrainingResult]

Agent: [1×1 rl.agent.rlLSPIAmericanOptionAgent]

Since R2026a

This example shows the workflow to price a Vanilla instrument with a "Bermudan" ExerciseStyle when using a Heston model and an AssetReinforcementLearning pricing method. Note, to use this functionality, you must have Reinforcement Learning Toolbox™ installed.

Create Vanilla Instrument Object

Use fininstrument to create a Vanilla instrument object.

VanillaOpt = fininstrument("Vanilla",ExerciseDate=[datetime(2019,1,16),datetime(2019,1,26)],Strike=110,OptionType="put",ExerciseStyle="bermudan",Name="vanilla_option")

VanillaOpt =

Vanilla with properties:

OptionType: "put"

ExerciseStyle: "bermudan"

ExerciseDate: [16-Jan-2019 26-Jan-2019]

Strike: [110 110]

Name: "vanilla_option"

Create Heston Model Object

Use finmodel to create a Heston model object.

HestonModel = finmodel("Heston",V0=0.032,ThetaV=0.1,Kappa=0.003,SigmaV=0.08,RhoSV=0.9)HestonModel =

Heston with properties:

V0: 0.0320

ThetaV: 0.1000

Kappa: 0.0030

SigmaV: 0.0800

RhoSV: 0.9000

Create ratecurve Object

Create a ratecurve object using ratecurve.

Settle = datetime(2019,1,1); Type = 'zero'; ZeroTimes = [calmonths(6) calyears([1 2 3 4 5 7 10 20 30])]'; ZeroRates = [0.0052 0.0055 0.0061 0.0073 0.0094 0.0119 0.0168 0.0222 0.0293 0.0307]'; ZeroDates = Settle + ZeroTimes; myRC = ratecurve('zero',Settle,ZeroDates,ZeroRates)

myRC =

ratecurve with properties:

Type: "zero"

Compounding: -1

Basis: 0

Dates: [10×1 datetime]

Rates: [10×1 double]

Settle: 01-Jan-2019

InterpMethod: "linear"

ShortExtrapMethod: "next"

LongExtrapMethod: "previous"

Create AssetReinforcementLearning Pricer Object

Use finpricer to create an AssetReinforcementLearning pricer object and use the ratecurve object for the 'DiscountCurve' name-value pair argument.

SpotPrice = 100;

SimDates = [Settle+days(1):days(2):Settle+calmonths(1)];

outPricer = finpricer("AssetReinforcementLearning",DiscountCurve=myRC,Model=HestonModel,SpotPrice=SpotPrice,SimulationDates=SimDates)outPricer =

AssetReinforcementLearning with properties:

DiscountCurve: [1×1 ratecurve]

SpotPrice: 100

SimulationDates: [02-Jan-2019 04-Jan-2019 06-Jan-2019 08-Jan-2019 10-Jan-2019 12-Jan-2019 14-Jan-2019 16-Jan-2019 18-Jan-2019 20-Jan-2019 22-Jan-2019 24-Jan-2019 26-Jan-2019 28-Jan-2019 … ] (1×16 datetime)

NumTrials: 1000

Model: [1×1 finmodel.Heston]

DividendType: "continuous"

DividendValue: 0

Price Vanilla Instrument

Use price to compute the price for the Vanilla instrument.

[Price,priceResultData] = price(outPricer,VanillaOpt)

Price = 10.1096

priceResultData =

priceresult with properties:

Results: [1×1 table]

PricerData: [1×1 struct]

priceResultData.PricerData

ans = struct with fields:

SimulationTimes: [17×1 timetable]

Paths: [17×2×1000 double]

TrainingStats: [1×1 rl.train.result.rlTrainingResult]

Agent: [1×1 rl.agent.rlLSPIAmericanOptionAgent]

More About

Tips

After creating a Vanilla instrument object, you can use setExercisePolicy to

change the size of the options. For example, if you have the following

instrument:

VanillaOpt = fininstrument("Vanilla",'ExerciseDate',datetime(2021,5,1),'Strike',29,'OptionType',"put",'ExerciseStyle',"European")Vanilla instrument's size by changing the

ExerciseStyle from "European" to

"American", use setExercisePolicy:VanillaOpt = setExercisePolicy(VanillaOpt,[datetime(2021,1,1) datetime(2022,1,1)],100,'American')

Version History

Introduced in R2020aSee Also

Functions

Topics

- Price European Vanilla Call Options Using Black-Scholes Model and Different Equity Pricers

- Use Black-Scholes Model to Price Asian Options with Several Equity Pricers

- Get Started with Workflows Using Object-Based Framework for Pricing Financial Instruments

- Choose Instruments, Models, and Pricers

- Supported Exercise Styles