Compute Maximum Reward-to-Risk Ratio for CVaR Portfolio

Create a PortfolioCVaR object and incorporate a list of assets from CAPMUniverse.mat. Use simulateNormalScenariosByData to simulate the scenarios for each of the assets. These portfolio constraints require fully invested long-only portfolios (nonnegative weights that must sum to 1).

rng(1) % Set the seed for reproducibility. load CAPMuniverse p = PortfolioCVaR('AssetList',Assets(1:12)); p = simulateNormalScenariosByData(p, Data(:,1:12), 20000 ,'missingdata',true); p = setProbabilityLevel(p, 0.95); p = setDefaultConstraints(p); disp(p)

PortfolioCVaR with properties:

BuyCost: []

SellCost: []

RiskFreeRate: []

ProbabilityLevel: 0.9500

Turnover: []

BuyTurnover: []

SellTurnover: []

NumScenarios: 20000

Name: []

NumAssets: 12

AssetList: {'AAPL' 'AMZN' 'CSCO' 'DELL' 'EBAY' 'GOOG' 'HPQ' 'IBM' 'INTC' 'MSFT' 'ORCL' 'YHOO'}

InitPort: []

AInequality: []

bInequality: []

AEquality: []

bEquality: []

LowerBound: [12×1 double]

UpperBound: []

LowerBudget: 1

UpperBudget: 1

GroupMatrix: []

LowerGroup: []

UpperGroup: []

GroupA: []

GroupB: []

LowerRatio: []

UpperRatio: []

MinNumAssets: []

MaxNumAssets: []

ConditionalBudgetThreshold: []

ConditionalUpperBudget: []

BoundType: [12×1 categorical]

To obtain the portfolio that maximizes the reward-to-risk ratio (which is equivalent to the Sharpe ratio for mean-variance portfolios), search on the efficient frontier iteratively for the portfolio that minimizes the negative of the reward-to-risk ratio:

To do so, use the sratio function, defined in the Local Functions section, to return the negative reward-to-risk ratio for a target return. Then, pass this function to fminbnd. fminbnd iterates through the possible return values and evaluates their associated reward-to-risk ratio. fminbnd returns the optimal return for which the maximum reward-to-risk ratio is achieved (or that minimizes the negative of the reward-to-risk ratio).

% Obtain the minimum and maximum returns of the portfolio. pwgtLimits = estimateFrontierLimits(p); retLimits = estimatePortReturn(p,pwgtLimits); minret = retLimits(1); maxret = retLimits(2); % Search on the frontier iteratively. Find the return that minimizes the % negative of the reward-to-risk ratio. fhandle = @(ret) iterative_local_obj(ret,p); options = optimset('Display', 'off', 'TolX', 1.0e-8); optret = fminbnd(fhandle, minret, maxret, options); % Obtain the portfolio weights associated with the return that achieves % the maximum reward-to-risk ratio. pwgt = estimateFrontierByReturn(p,optret)

pwgt = 12×1

0.0885

0

0

0

0

0.9115

0

0

0

0

0

0

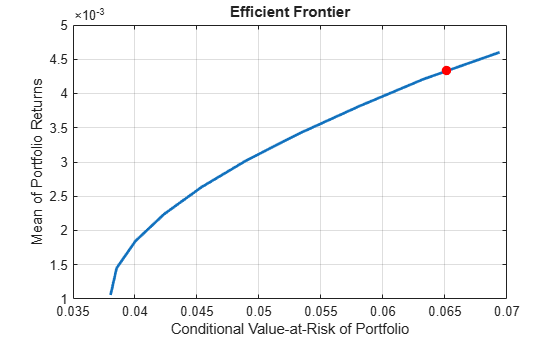

Use plotFrontier to plot the efficient frontier and estimatePortRisk to estimate the maximum reward-to-risk ratio portfolio.

plotFrontier(p); hold on % Compute the risk level for the maximum reward-to-risk ratio portfolio. optrsk = estimatePortRisk(p,pwgt); scatter(optrsk,optret,50,'red','filled') hold off

Local Functions

This local function that computes the negative of the reward-to-risk ratio for a target return level.

function sratio = iterative_local_obj(ret, obj) % Set the objective function to the negative of the reward-to-risk ratio. risk = estimatePortRisk(obj,estimateFrontierByReturn(obj,ret)); if ~isempty(obj.RiskFreeRate) sratio = -(ret - obj.RiskFreeRate)/risk; else sratio = -ret/risk; end end

See Also

PortfolioCVaR | getScenarios | setScenarios | estimateScenarioMoments | simulateNormalScenariosByMoments | simulateNormalScenariosByData | setCosts | checkFeasibility

Topics

- Troubleshooting CVaR Portfolio Optimization Results

- Creating the PortfolioCVaR Object

- Working with CVaR Portfolio Constraints Using Defaults

- Asset Returns and Scenarios Using PortfolioCVaR Object

- Estimate Efficient Portfolios for Entire Frontier for PortfolioCVaR Object

- Estimate Efficient Frontiers for PortfolioCVaR Object

- Hedging Using CVaR Portfolio Optimization

- PortfolioCVaR Object

- Portfolio Optimization Theory

- PortfolioCVaR Object Workflow