VAR Model Case Study

This example shows how to analyze a VAR model.

Overview of Case Study

This section contains an example of the workflow described in VAR Model Workflow. The example uses three time series: GDP, M1 money supply, and the 3-month T-bill rate. The example shows:

Loading and transforming the data for stationarity

Partitioning the transformed data into presample, estimation, and forecast intervals to support a backtesting experiment

Making several models

Fitting the models to the data

Deciding which of the models is best

Making forecasts based on the best model

Load and Transform Data

The file Data_USEconModel ships with Econometrics Toolbox™ software. The file contains time series from the Federal Reserve Bank of St. Louis Economics Data (FRED) database in a tabular array. This example uses three of the time series:

GDP (

GDP)M1 money supply (

M1SL)3-month T-bill rate (

TB3MS)

Load the data set. Create a variable for real GDP.

load Data_USEconModel

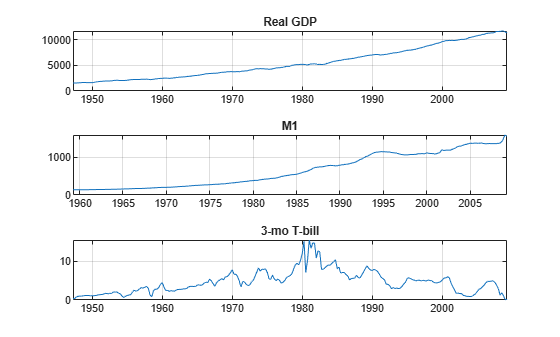

DataTimeTable.RGDP = DataTimeTable.GDP./DataTimeTable.GDPDEF*100;Plot the data to look for trends.

figure tiledlayout(3,1) nexttile plot(DataTimeTable.Time,DataTimeTable.RGDP); title("Real GDP") grid on nexttile plot(DataTimeTable.Time,DataTimeTable.M1SL); title("M1") grid on nexttile plot(DataTimeTable.Time,DataTimeTable.TB3MS) title("3-mo T-bill") grid on

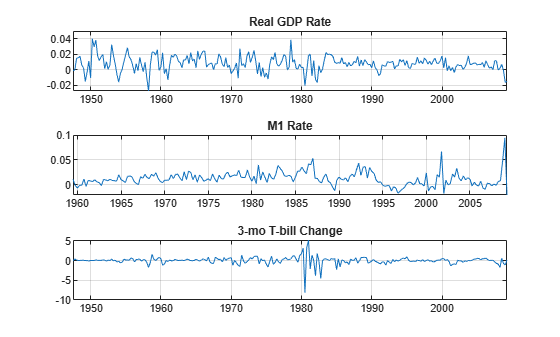

The real GDP and M1 data appear to grow exponentially, while the T-bill returns show no exponential growth. To counter the trends in real GDP and M1, take a difference of the logarithms of the data. Also, stabilize the T-bill series by taking the first difference. Synchronize the date series so that the data has the same number of rows for each column.

rgdpg = price2ret(DataTimeTable.RGDP); m1slg = price2ret(DataTimeTable.M1SL); dtb3ms = diff(DataTimeTable.TB3MS); Data = array2timetable([rgdpg m1slg dtb3ms],... RowTimes=DataTimeTable.Time(2:end),VariableNames=["RGDPRate" "M1SLRate" "TB3MSChng"]); seriesnames = ["Real GDP Rate","M1 Rate","3-mo T-bill Change"]; figure tiledlayout(3,1) for j = 1:3 nexttile plot(Data.Time,Data{:,j}); title(seriesnames(j)) grid on end

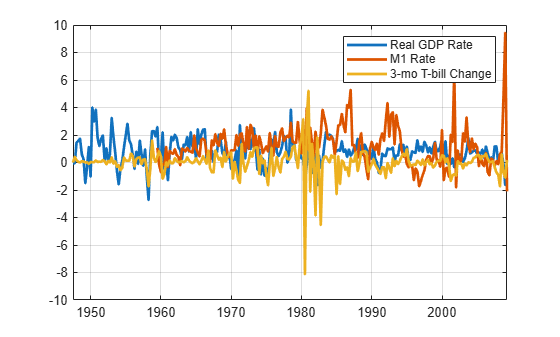

The scale of the first two columns is about 100 times smaller than the third. Multiply the first two columns by 100 so that the time series are all roughly on the same scale. This scaling makes it easy to plot all the series on the same plot. More importantly, this type of scaling makes optimizations more numerically stable (for example, maximizing loglikelihoods).

Data{:,1:2} = 100*Data{:,1:2};

figure

plot(Data.Time,Data.Variables,LineWidth=2);

grid on

legend(seriesnames)

Select and Fit the Models

You can select many different models for the data. This example uses four models.

VAR(2) with diagonal autoregressive

VAR(2) with full autoregressive

VAR(4) with diagonal autoregressive

VAR(4) with full autoregressive

Remove all missing values from the beginning of the series.

Data = rmmissing(Data);

Create the four models.

numseries = 3;

dnan = diag(nan(numseries,1));

VAR2diag = varm(AR={dnan dnan},SeriesNames=seriesnames);

VAR2full = varm(numseries,2);

VAR2full.SeriesNames = seriesnames;

VAR4diag = varm(AR={dnan dnan dnan dnan},SeriesNames=seriesnames);

VAR4full = varm(numseries,4);

VAR4full.SeriesNames = seriesnames;The matrix dnan is a diagonal matrix with NaN values along its main diagonal. In general, missing values specify the presence of the parameter in the model, and indicate that the parameter needs to be fit to data. MATLAB® holds the off diagonal elements, 0, fixed during estimation. In contrast, the specifications for VAR2full and VAR4full have matrices composed of NaN values. Therefore, estimate fits full matrices for autoregressive matrices.

To assess the quality of the models, create index vectors that divide the response data into three periods: presample, estimation, and forecast. Fit the models to the estimation data, using the presample period to provide lagged data. Compare the predictions of the fitted models to the forecast data. The estimation period is in sample, and the forecast period is out of sample (also known as backtesting).

For the two VAR(4) models, the presample period is the first four rows of Data. Use the same presample period for the VAR(2) models so that all the models are fit to the same data. This is necessary for model fit comparisons. For both models, the forecast period is the final 10% of the rows of Data. The estimation period for the models goes from row 5 to the 90% row. Define these data periods.

idxPre = 1:4; T = ceil(.9*size(Data,1)); idxEst = 5:T; idxF = (T+1):size(Data,1); fh = numel(idxF);

Now that the models and time series exist, you can easily fit the models to the data.

[EstMdl1,EstSE1,logL1,E1] = estimate(VAR2diag,Data{idxEst,:}, ...

Y0=Data{idxPre,:});

[EstMdl2,EstSE2,logL2,E2] = estimate(VAR2full,Data{idxEst,:}, ...

Y0=Data{idxPre,:});

[EstMdl3,EstSE3,logL3,E3] = estimate(VAR4diag,Data{idxEst,:}, ...

Y0=Data{idxPre,:});

[EstMdl4,EstSE4,logL4,E4] = estimate(VAR4full,Data{idxEst,:}, ...

Y0=Data{idxPre,:});The

EstMdlmodel objects are the fitted models.The

EstSEstructures contain the standard errors of the fitted models.The

logLvalues are the loglikelihoods of the fitted models, which you use to help select the best model.The

Evectors are the residuals, which are the same size as the estimation data.

Check Model Adequacy

You can check whether the estimated models are stable and invertible by displaying the Description property of each object. (There are no MA terms in these models, so the models are necessarily invertible.) The descriptions show that all the estimated models are stable.

EstMdl1.Description

ans = "AR-Stationary 3-Dimensional VAR(2) Model"

EstMdl2.Description

ans = "AR-Stationary 3-Dimensional VAR(2) Model"

EstMdl3.Description

ans = "AR-Stationary 3-Dimensional VAR(4) Model"

EstMdl4.Description

ans = "AR-Stationary 3-Dimensional VAR(4) Model"

AR-Stationary appears in the output indicating that the autoregressive processes are stable.

You can compare the restricted (diagonal) AR models to their unrestricted (full) counterparts using lratiotest. The test rejects or fails to reject the hypothesis that the restricted models are adequate, with a default 5% tolerance. This is an in-sample test.

Apply the likelihood ratio tests. You must extract the number of estimated parameters from the summary structure returned by summarize. Then, pass the differences in the number of estimated parameters and the loglikelihoods to lratiotest to perform the tests.

results1 = summarize(EstMdl1); np1 = results1.NumEstimatedParameters; results2 = summarize(EstMdl2); np2 = results2.NumEstimatedParameters; results3 = summarize(EstMdl3); np3 = results3.NumEstimatedParameters; results4 = summarize(EstMdl4); np4 = results4.NumEstimatedParameters; reject1 = lratiotest(logL2,logL1,np2 - np1)

reject1 = logical

1

reject3 = lratiotest(logL4,logL3,np4 - np3)

reject3 = logical

1

reject4 = lratiotest(logL4,logL2,np4 - np2)

reject4 = logical

0

The 1 results indicate that the likelihood ratio test rejected both the restricted models in favor of the corresponding unrestricted models. Therefore, based on this test, the unrestricted VAR(2) and VAR(4) models are preferable. However, the test does not reject the unrestricted VAR(2) model in favor of the unrestricted VAR(4) model. (This test regards the VAR(2) model as an VAR(4) model with restrictions that the autoregression matrices AR(3) and AR(4) are 0.) Therefore, it seems that the unrestricted VAR(2) model is the best model.

To find the best model in a set, minimize the Akaike information criterion (AIC). Use in-sample data to compute the AIC. Calculate the criterion for the four models.

AIC = aicbic([logL1 logL2 logL3 logL4],[np1 np2 np3 np4])

AIC = 1×4

103 ×

1.4794 1.4396 1.4785 1.4537

The best model according to this criterion is the unrestricted VAR(2) model. Notice, too, that the unrestricted VAR(4) model has lower Akaike information than either of the restricted models. Based on this criterion, the unrestricted VAR(2) model is best, with the unrestricted VAR(4) model coming next in preference.

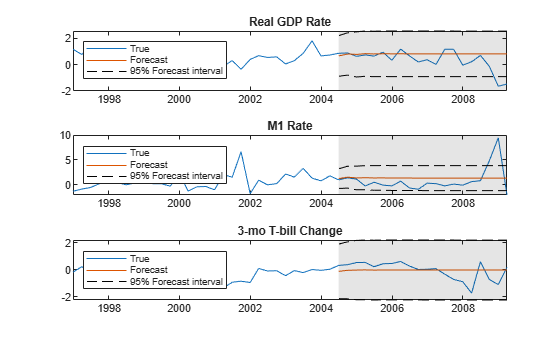

To compare the predictions of the four models against the forecast data, use forecast. This function returns both a prediction of the mean time series, and an error covariance matrix that gives confidence intervals about the means. This is an out-of-sample calculation.

[FY1,FYCov1] = forecast(EstMdl1,fh,Data{idxEst,:});

[FY2,FYCov2] = forecast(EstMdl2,fh,Data{idxEst,:});

[FY3,FYCov3] = forecast(EstMdl3,fh,Data{idxEst,:});

[FY4,FYCov4] = forecast(EstMdl4,fh,Data{idxEst,:});Estimate approximate 95% forecast intervals for the best fitting model.

extractMSE = @(x)diag(x)'; MSE = cellfun(extractMSE,FYCov2,UniformOutput=false); SE = sqrt(cell2mat(MSE)); YFI = zeros(fh,EstMdl2.NumSeries,2); YFI(:,:,1) = FY2 - 2*SE; YFI(:,:,2) = FY2 + 2*SE;

This plot shows the predictions of the best fitting model in the shaded region to the right.

figure tiledlayout(3,1) for j = 1:EstMdl2.NumSeries nexttile h1 = plot(Data.Time((end-49):end),Data{(end-49):end,j}); hold on h2 = plot(Data.Time(idxF),FY2(:,j)); h3 = plot(Data.Time(idxF),YFI(:,j,1),"k--"); plot(Data.Time(idxF),YFI(:,j,2),"k--"); title(EstMdl2.SeriesNames{j}) h = gca; fill([Data.Time(idxF(1)) h.XLim([2 2]) Data.Time(idxF(1))], ... h.YLim([1 1 2 2]),"k",FaceAlpha=0.1,EdgeColor="none"); legend([h1 h2 h3],"True","Forecast","95% Forecast interval", ... Location="northwest") hold off end

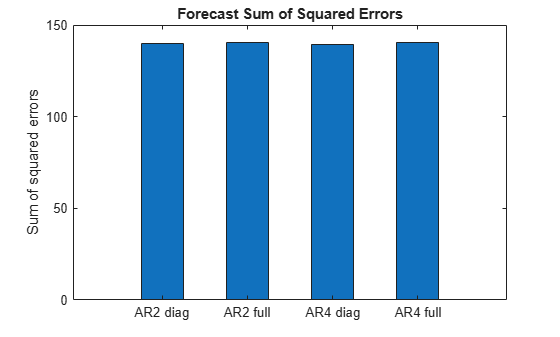

Calculate the sum-of-squares error between the predictions and the data.

Error1 = Data{idxF,:} - FY1;

Error2 = Data{idxF,:} - FY2;

Error3 = Data{idxF,:} - FY3;

Error4 = Data{idxF,:} - FY4;

SSerror1 = Error1(:)' * Error1(:);

SSerror2 = Error2(:)' * Error2(:);

SSerror3 = Error3(:)' * Error3(:);

SSerror4 = Error4(:)' * Error4(:);

figure

bar([SSerror1 SSerror2 SSerror3 SSerror4],.5)

ylabel("Sum of squared errors")

set(gca,XTickLabel=["AR2 diag" "AR2 full" "AR4 diag" "AR4 full"])

title("Forecast Sum of Squared Errors")

The predictive performances of the four models are similar.

The full AR(2) model seems to be the best and most parsimonious fit. Its model parameters are as follows.

summarize(EstMdl2)

AR-Stationary 3-Dimensional VAR(2) Model

Effective Sample Size: 176

Number of Estimated Parameters: 21

LogLikelihood: -698.801

AIC: 1439.6

BIC: 1506.18

Value StandardError TStatistic PValue

__________ _____________ __________ __________

Constant(1) 0.34832 0.11527 3.0217 0.0025132

Constant(2) 0.55838 0.1488 3.7526 0.00017502

Constant(3) -0.45434 0.15245 -2.9803 0.0028793

AR{1}(1,1) 0.26252 0.07397 3.5491 0.00038661

AR{1}(2,1) -0.029371 0.095485 -0.3076 0.75839

AR{1}(3,1) 0.22324 0.097824 2.2821 0.022484

AR{1}(1,2) -0.074627 0.054476 -1.3699 0.17071

AR{1}(2,2) 0.2531 0.070321 3.5992 0.00031915

AR{1}(3,2) -0.017245 0.072044 -0.23936 0.81082

AR{1}(1,3) 0.032692 0.056182 0.58189 0.56064

AR{1}(2,3) -0.35827 0.072523 -4.94 7.8112e-07

AR{1}(3,3) -0.29179 0.0743 -3.9272 8.5943e-05

AR{2}(1,1) 0.21378 0.071283 2.9991 0.0027081

AR{2}(2,1) -0.078493 0.092016 -0.85304 0.39364

AR{2}(3,1) 0.24919 0.094271 2.6433 0.0082093

AR{2}(1,2) 0.13137 0.051691 2.5415 0.011038

AR{2}(2,2) 0.38189 0.066726 5.7233 1.045e-08

AR{2}(3,2) 0.049403 0.068361 0.72269 0.46987

AR{2}(1,3) -0.22794 0.059203 -3.85 0.00011809

AR{2}(2,3) -0.0052932 0.076423 -0.069262 0.94478

AR{2}(3,3) -0.37109 0.078296 -4.7397 2.1408e-06

Innovations Covariance Matrix:

0.5931 0.0611 0.1705

0.0611 0.9882 -0.1217

0.1705 -0.1217 1.0372

Innovations Correlation Matrix:

1.0000 0.0798 0.2174

0.0798 1.0000 -0.1202

0.2174 -0.1202 1.0000

Forecast Observations

You can make predictions or forecasts using the fitted model (EstMdl2) either by:

Calling

forecastand passing the last few rows ofYFSimulating several time series with

simulate

In both cases, transform the forecasts so they are directly comparable to the original time series.

Generate 10 predictions from the fitted model beginning at the latest times using forecast.

[YPred,YCov] = forecast(EstMdl2,10,Data{idxF,:});Transform the predictions by undoing the scaling and differencing applied to the original data. Make sure to insert the last observation at the beginning of the time series before using cumsum to undo the differencing. And, since differencing occurred after taking logarithms, insert the logarithm before using cumsum.

YFirst = DataTimeTable(:,["RGDP" "M1SL" "TB3MS"]); EndPt = YFirst{end,:}; EndPt(:,1:2) = log(EndPt(:,1:2)); YPred(:,1:2) = YPred(:,1:2)/100; % Rescale percentage YPred = [EndPt; YPred]; % Prepare for cumsum YPred = cumsum(YPred); YPred(:,1:2) = exp(YPred(:,1:2)); fdates = dateshift(YFirst.Time(end),"end","quarter",0:10); % Insert forecast horizon figure tiledlayout(3,1) for j = 1:EstMdl2.NumSeries nexttile plot(fdates,YPred(:,j),"--b") hold on plot(YFirst.Time,YFirst{:,j},"k") grid on title(EstMdl2.SeriesNames{j}) h = gca; fill([fdates(1) h.XLim([2 2]) fdates(1)],h.YLim([1 1 2 2]),"k", ... FaceAlpha=0.1,EdgeColor="none"); hold off end

The plots show the extrapolations as blue dashed lines in the light gray forecast horizon, and the original data series in solid black.

Look at the last few years in this plot to get a sense of how the predictions relate to the latest data points.

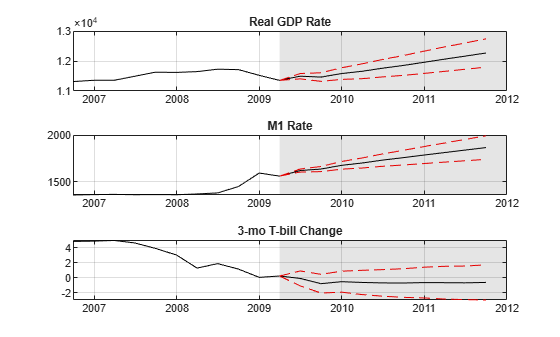

YLast = YFirst(170:end,:); figure tiledlayout(3,1) for j = 1:EstMdl2.NumSeries nexttile plot(fdates,YPred(:,j),"b--") hold on plot(YLast.Time,YLast{:,j},"k") grid on title(EstMdl2.SeriesNames{j}) h = gca; fill([fdates(1) h.XLim([2 2]) fdates(1)],h.YLim([1 1 2 2]),"k", ... FaceAlpha=0.1,EdgeColor="none"); hold off end

The forecast shows increasing real GDP and M1, and a slight decline in the interest rate. However, the forecast has no error bars.

Alternatively, you can generate 10 predictions from the fitted model beginning at the latest times using simulate. This method simulates 2000 time series times, and then generates the means and standard deviations for each period. The means of the deviates for each period are the predictions for that period.

Simulate a time series from the fitted model beginning at the latest times.

rng(1); % For reproducibility

YSim = simulate(EstMdl2,10,Y0=Data{idxF,:},NumPaths=2000);Transform the predictions by undoing the scaling and differencing applied to the original data. Make sure to insert the last observation at the beginning of the time series before using cumsum to undo the differencing. And, since differencing occurred after taking logarithms, insert the logarithm before using cumsum.

EndPt = YFirst{end,:};

EndPt(1:2) = log(EndPt(1:2));

YSim(:,1:2,:) = YSim(:,1:2,:)/100;

YSim = [repmat(EndPt,[1,1,2000]);YSim];

YSim(:,1:3,:) = cumsum(YSim(:,1:3,:));

YSim(:,1:2,:) = exp(YSim(:,1:2,:));Compute the mean and standard deviation of each series, and plot the results. The plot has the mean in black, with a +/- 1 standard deviation in red.

YMean = mean(YSim,3); YSTD = std(YSim,0,3); figure tiledlayout(3,1) for j = 1:EstMdl2.NumSeries nexttile plot(fdates,YMean(:,j),"k") grid on hold on plot(YLast.Time(end-10:end),YLast{end-10:end,j},"k") plot(fdates,YMean(:,j) + YSTD(:,j),"--r") plot(fdates,YMean(:,j) - YSTD(:,j),"--r") title(EstMdl2.SeriesNames{j}) h = gca; fill([fdates(1) h.XLim([2 2]) fdates(1)],h.YLim([1 1 2 2]),"k", ... FaceAlpha=0.1,EdgeColor="none"); hold off end

The plots show increasing growth in GDP, moderate to little growth in M1, and uncertainty about the direction of T-bill rates.

See Also

Objects

Functions

estimate|forecast|simulate|lratiotest|aicbic