price2ret

Convert prices to returns

Syntax

Description

ReturnTbl = price2ret(PriceTbl)DataVariables name-value argument. (since R2022a)

[___] = price2ret(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name=Value)price2ret returns the output argument combination for the

corresponding input arguments. For example,

price2ret(Tbl,Method="periodic",DataVariables=1:5) computes the simple

periodic returns of the first five variables in the input table

Tbl. (since R2022a)

Examples

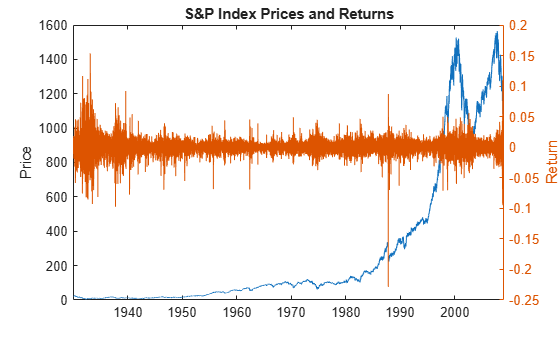

Load the Schwert Stock data set Data_SchwertStock.mat, which contains daily prices of the S&P index from 1930 through 2008, among other variables (enter Description for more details).

load Data_SchwertStock

numObs = height(DataTableDly)numObs = 20838

dates = datetime(datesDly,ConvertFrom="datenum");Convert the S&P price series to returns.

prices = DataTableDly.SP; returns = price2ret(prices);

returns is a 20837-by-1 vector of daily S&P returns compounded continuously.

r9 = returns(9)

r9 = 0.0033

p9_10 = [prices(9) prices(10)]

p9_10 = 1×2

21.4500 21.5200

returns(9) = 0.0033 is the daily return of the prices in the interval [21.45, 21.52].

plot(dates,DataTableDly.SP) ylabel("Price") yyaxis right plot(dates(1:end-1),returns) ylabel("Return") title("S&P Index Prices and Returns")

Since R2022a

Convert the price series in a table to simple periodic return series.

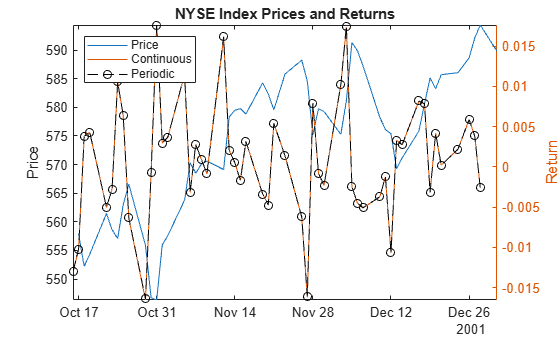

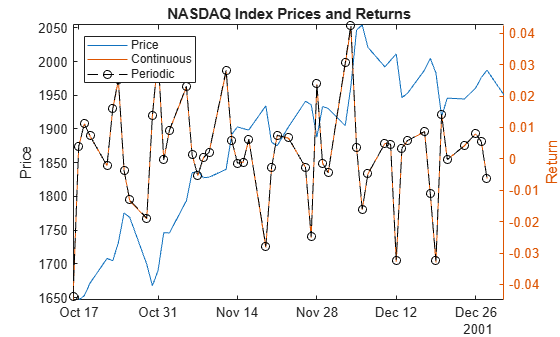

Load the US equity indices data set, which contains the table DataTable of daily closing prices of the NYSE and NASDAQ composite indices from 1990 through 2011.

load Data_EquityIdxCreate a timetable from the table.

dates = datetime(dates,ConvertFrom="datenum");

TT = table2timetable(DataTable,RowTimes=dates);

numObs = height(TT);Convert the NASDAQ and NYSE prices to simple periodic and continuously compounded returns.

varnames = ["NASDAQ" "NYSE"]; TTRetC = price2ret(TT,DataVariables=varnames); TTRetP = price2ret(TT,DataVariables=varnames,Method="periodic");

Because TT is a timetable, TTRetC and TTRetP are timetables.

Plot the return series with the corresponding prices for the last 50 observations.

idx = ((numObs - 1) - 51):(numObs - 1); figure plot(dates(idx + 1),TT.NYSE(idx + 1)) title("NYSE Index Prices and Returns") ylabel("Price") yyaxis right h = plot(dates(idx),[TTRetC.NYSE(idx) TTRetP.NYSE(idx)]); h(2).Marker = 'o'; h(2).Color = 'k'; ylabel("Return") legend(["Price" "Continuous" "Periodic"],Location="northwest") axis tight

figure plot(dates(idx + 1),TT.NASDAQ(idx + 1)) title("NASDAQ Index Prices and Returns") ylabel("Price") yyaxis right h = plot(dates(idx),[TTRetC.NASDAQ(idx) TTRetP.NASDAQ(idx)]); h(2).Marker = 'o'; h(2).Color = 'k'; ylabel("Return") legend(["Price" "Continuous" "Periodic"],Location="northwest") axis tight

In this case, the simple periodic and continuously compounded returns of each price series are similar.

Since R2022a

Create two stock price series from continuously compounded returns that have the following characteristics:

Series 1 grows at a 10 percent rate at each observation time.

Series 2 changes at a random uniform rate in the interval [-0.1, 0.1] at each observation time.

Each series starts at price 100 and is 10 observations in length.

rng(1); % For reproducibility

numObs = 10;

p1 = 100;

r1 = 0.10;

r2 = [0; unifrnd(-0.10,0.10,numObs - 1,1)];

s1 = 100*exp(r1*(0:(numObs - 1))');

cr2 = cumsum(r2);

s2 = 100*exp(cr2);

S = [s1 s2];Convert each price series to a return series, and return the observation intervals.

[R,intervals] = price2ret(S);

Prepend the return series so that the input and output elements are of the same length and correspond.

[[NaN; intervals] S [[NaN NaN]; R] r2]

ans = 10×6

NaN 100.0000 100.0000 NaN NaN 0

1.0000 110.5171 98.3541 0.1000 -0.0166 -0.0166

1.0000 122.1403 102.7850 0.1000 0.0441 0.0441

1.0000 134.9859 93.0058 0.1000 -0.1000 -0.1000

1.0000 149.1825 89.4007 0.1000 -0.0395 -0.0395

1.0000 164.8721 83.3026 0.1000 -0.0706 -0.0706

1.0000 182.2119 76.7803 0.1000 -0.0815 -0.0815

1.0000 201.3753 72.1105 0.1000 -0.0627 -0.0627

1.0000 222.5541 69.9172 0.1000 -0.0309 -0.0309

1.0000 245.9603 68.4885 0.1000 -0.0206 -0.0206

price2ret returns rates matching the rates from the simulated series. price2ret assumes prices are recorded in a regular time base. Therefore, all durations between prices are 1.

Convert the prices to returns again, but associate the prices with years starting from August 1, 2010.

tau1 = datetime(2010,08,01); dates = tau1 + years((0:(numObs-1))'); [Ry,intervalsy] = price2ret(S,Ticks=dates); [[NaN; intervalsy] S [[NaN NaN]; Ry] r2]

ans = 10×6

NaN 100.0000 100.0000 NaN NaN 0

365.2425 110.5171 98.3541 0.0003 -0.0000 -0.0166

365.2425 122.1403 102.7850 0.0003 0.0001 0.0441

365.2425 134.9859 93.0058 0.0003 -0.0003 -0.1000

365.2425 149.1825 89.4007 0.0003 -0.0001 -0.0395

365.2425 164.8721 83.3026 0.0003 -0.0002 -0.0706

365.2425 182.2119 76.7803 0.0003 -0.0002 -0.0815

365.2425 201.3753 72.1105 0.0003 -0.0002 -0.0627

365.2425 222.5541 69.9172 0.0003 -0.0001 -0.0309

365.2425 245.9603 68.4885 0.0003 -0.0001 -0.0206

price2ret assumes time units are days. Therefore, all durations are approximately 365 and the returns are normalized for that time unit.

Compute returns again, but specify that the observation times are years.

[Ryy,intervalsyy] = price2ret(S,Ticks=dates,Units="years");

[[NaN; intervalsyy] S [[NaN NaN]; Ryy] r2]ans = 10×6

NaN 100.0000 100.0000 NaN NaN 0

1.0000 110.5171 98.3541 0.1000 -0.0166 -0.0166

1.0000 122.1403 102.7850 0.1000 0.0441 0.0441

1.0000 134.9859 93.0058 0.1000 -0.1000 -0.1000

1.0000 149.1825 89.4007 0.1000 -0.0395 -0.0395

1.0000 164.8721 83.3026 0.1000 -0.0706 -0.0706

1.0000 182.2119 76.7803 0.1000 -0.0815 -0.0815

1.0000 201.3753 72.1105 0.1000 -0.0627 -0.0627

1.0000 222.5541 69.9172 0.1000 -0.0309 -0.0309

1.0000 245.9603 68.4885 0.1000 -0.0206 -0.0206

price2ret normalizes the returns relative to years, and now the returned rates match the simulated rates.

Input Arguments

Name-Value Arguments

Output Arguments

Algorithms

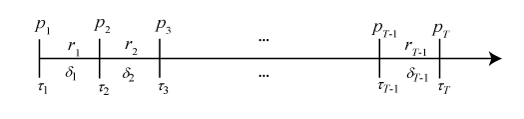

Consider the following variables:

The following figure shows how the inputs and outputs are associated.