hpfilter

Hodrick-Prescott filter for trend and cyclical components

Syntax

Description

The hpfilter function applies the Hodrick-Prescott filter to

separate one or more time series into additive trend and cyclical components.

hpfilter optionally plots the series and trend component, with

cycles removed. The plot helps you select a smoothing parameter.

In addition to the Hodrick-Prescott filter, Econometrics Toolbox™ supports the Baxter-King (bkfilter),

Christiano-Fitzgerald (cffilter), and

Hamilton (hfilter)

filters.

[

returns tables or timetables containing variables for the trend and cyclical components

from applying the Hodrick-Prescott filter to each variable in the input table or

timetable. To select different variables to filter, use the

TTbl,CTbl] = hpfilter(Tbl)DataVariables name-value argument. (since R2022a)

[___] = hpfilter(___,

specifies options using one or more name-value arguments in

addition to any of the input argument combinations in previous syntaxes.

Name=Value)hpfilter returns the output argument combination for the

corresponding input arguments. For example,

hpfilter(Tbl,Smoothing=100,DataVariables=1:5) applies the

Hodrick-Prescott filter to the first five variables in the input table

Tbl and sets the smoothing parameter to

100. (since R2022a)

hpfilter(___) plots time series variables in the

input data and their respective trend components, computed by the Hodrick-Prescott filter,

on the same axes.

hpfilter(

plots on the axes specified by ax,___)ax instead of

the current axes (gca). ax can precede any of the input

argument combinations in the previous syntaxes. (since R2022a)

Examples

Plot the cyclical component of the US post-WWII, seasonally adjusted, quarterly, real gross national product (GNPR).

load Data_GNP

GNPR = Data(:,2);

[trend,cyclical] = hpfilter(GNPR);

T = numel(trend)T = 235

trend and cyclical are 235-by-1 vectors containing the trend and cyclical components, respectively, resulting from applying the Hodrick-Prescott filter to the series with default smoothing parameter 1600.

plot(dates,cyclical) axis tight ylabel("Real GNP Cyclical Component")

Since R2022a

Apply the Hodrick-Prescott filter to all variables in input table variables.

Load the Schwert stock data set Data_SchwertStock.mat, which contains monthly returns of the NYSE index from 1871 through 2008 in DataTimeTableMth, among three other variables (for details, enter Description). Remove all missing observations from all series.

load Data_SchwertStock

TTM = rmmissing(DataTimeTableMth);Aggregate the monthly data in the timetable to quarterly measurements.

TTQ = convert2quarterly(TTM);

Apply the Hodrick-Prescott filter to all variables in the quarterly timetable. The default smoothing parameter value is 1600. Display the last few observed components.

[TQTT,CQTT] = hpfilter(TTQ); size(TQTT)

ans = 1×2

220 4

tail(TQTT)

Time Return DivYld CapGain CapGainA

___________ _________ _________ ___________ ___________

31-Mar-1924 0.0046179 0.0067678 -0.0021499 -0.0021499

30-Jun-1924 0.005586 0.0067204 -0.0011344 -0.0011344

30-Sep-1924 0.0066431 0.0066689 -2.5812e-05 -2.5812e-05

31-Dec-1924 0.0077772 0.0066142 0.0011629 0.0011629

31-Mar-1925 0.0089687 0.0065574 0.0024113 0.0024113

30-Jun-1925 0.010231 0.0064998 0.0037314 0.0037314

30-Sep-1925 0.011543 0.0064423 0.0051005 0.0051005

31-Dec-1925 0.012878 0.0063854 0.0064922 0.0064922

tail(CQTT)

Time Return DivYld CapGain CapGainA

___________ __________ ___________ __________ __________

31-Mar-1924 -0.019683 0.00033141 -0.020014 -0.020014

30-Jun-1924 0.059151 5.7125e-05 0.059093 0.059093

30-Sep-1924 -0.011788 0.00044598 -0.012234 -0.012234

31-Dec-1924 0.052846 0.00052627 0.05232 0.05232

31-Mar-1925 -0.056652 -0.00078018 -0.055872 -0.055872

30-Jun-1925 -0.0069909 -0.0010415 -0.0059494 -0.0059494

30-Sep-1925 0.0052352 -0.0011402 0.0063755 0.0063755

31-Dec-1925 0.036713 0.00070754 0.036006 0.036006

TQTT and CQTT are 220-by-4 timetables containing the trend and cyclical components, respectively, of the series in TTQ. Variables in the input and output timetables correspond.

By default, hpfilter filters all variables in the input table or timetable. To select a subset of variables, set the DataVariables option.

To compare outputs between different tabular inputs, apply the Hodrick-Prescott filter to all variables in the table of monthly data DataTableMth and the timetable of monthly data TTM.

% Table input of daily data

DTM = rmmissing(DataTableMth);

[TMDT,CMDT] = hpfilter(DTM);

size(TMDT)ans = 1×2

656 4

tail(TMDT)

Return DivYld CapGain CapGainA

________ _________ ________ ________

May1925 0.02665 0.0045709 0.022079 0.022079

Jun1925 0.0275 0.004558 0.022942 0.022942

Jul1925 0.028372 0.0045491 0.023823 0.023823

Aug1925 0.02926 0.0045437 0.024716 0.024716

Sep1925 0.030152 0.004542 0.02561 0.02561

Oct1925 0.031049 0.004543 0.026506 0.026506

Nov1925 0.031941 0.0045461 0.027395 0.027395

Dec1925 0.032844 0.0045508 0.028293 0.028293

tail(CMDT)

Return DivYld CapGain CapGainA

__________ __________ _________ _________

May1925 0.039536 -0.0020878 0.041624 0.041624

Jun1925 -0.02426 0.00090028 -0.02516 -0.02516

Jul1925 -0.0095168 0.00066325 -0.01018 -0.01018

Aug1925 0.018948 -0.0018318 0.02078 0.02078

Sep1925 -0.013374 0.00076008 -0.014134 -0.014134

Oct1925 0.037148 9.6588e-05 0.037051 0.037051

Nov1925 -0.040405 -0.0017316 -0.038674 -0.038674

Dec1925 0.016747 0.0025421 0.014205 0.014205

% Timetable input of daily data

[TMTT,CMTT] = hpfilter(TTM);

size(TMTT)ans = 1×2

656 4

tail(TMTT)

Time Return DivYld CapGain CapGainA

___________ ________ _________ ________ ________

01-May-1925 0.02665 0.0045709 0.022079 0.022079

01-Jun-1925 0.0275 0.004558 0.022942 0.022942

01-Jul-1925 0.028372 0.0045491 0.023823 0.023823

01-Aug-1925 0.02926 0.0045437 0.024716 0.024716

01-Sep-1925 0.030152 0.004542 0.02561 0.02561

01-Oct-1925 0.031049 0.004543 0.026506 0.026506

01-Nov-1925 0.031941 0.0045461 0.027395 0.027395

01-Dec-1925 0.032844 0.0045508 0.028293 0.028293

tail(CMTT)

Time Return DivYld CapGain CapGainA

___________ __________ __________ _________ _________

01-May-1925 0.039536 -0.0020878 0.041624 0.041624

01-Jun-1925 -0.02426 0.00090028 -0.02516 -0.02516

01-Jul-1925 -0.0095168 0.00066325 -0.01018 -0.01018

01-Aug-1925 0.018948 -0.0018318 0.02078 0.02078

01-Sep-1925 -0.013374 0.00076008 -0.014134 -0.014134

01-Oct-1925 0.037148 9.6588e-05 0.037051 0.037051

01-Nov-1925 -0.040405 -0.0017316 -0.038674 -0.038674

01-Dec-1925 0.016747 0.0025421 0.014205 0.014205

Because the data is disaggregated, the outputs of the daily data have more rows than from the quarterly data. The filter results of the daily inputs are equal among the corresponding outputs, but hpfilter returns tables of results, instead of timetables, when you supply data in a table.

Since R2022a

Load the Nelson-Plosser macroeconomic data set Data_NelsonPlosser.mat, which contains series measured yearly in the table DataTable.

load Data_NelsonPlosserFilter the real and nominal GNP series, GNPR and GNPN, respectively. Plot the trend component with each series by additionally returning the vector of graphics objects. Set the smoothing parameter to 100, as suggested in [1] for yearly data.

[TTblHP,CTblHP,hHP] = hpfilter(DataTimeTable,Smoothing=100, ... DataVariables=["GNPR" "GNPN"]);

Filter the series again, but set the smoothing parameter to 6.25, which is the suggested smoothing parameter value in [3] for yearly data.

figure [TTblRU,CTblRU,hRU] = hpfilter(DataTimeTable,Smoothing=6.25, ... DataVariables=["GNPR" "GNPN"]);

The smoothed trend of the latter plot contains more higher frequency cycles than the former plot, and, therefore, the smoothed trend in the latter plot follows the data more tightly.

Experiment with the smoothing parameter value by filtering the series several more times and setting the smoothing parameter to 0, 10, 100, 1000, 10,000, and Inf. Plot each set of results by not returning any outputs.

smoothing = [10.^(0:4) Inf]; tiledlayout(2,3) for j = 1:numel(smoothing) nexttile hpfilter(DataTimeTable,Smoothing=smoothing(j), ... DataVariables=["GNPR" "GNPN"]); title("\lambda = " + string(smoothing(j))); legend("off") end

Input Arguments

Name-Value Arguments

Output Arguments

More About

The Hodrick-Prescott filter decomposes an

observed time series yt (Y)

into a trend component τt

(Trend) and a cyclical component

ct (Cyclical) such that

yt =

τt +

ct. The method implements a high-pass filter for

the cycle that penalizes variations in the trend to a degree determined by the smoothing

parameter [1].

The objective function of the filter is

where:

T is the sample size.

λ is the smoothing parameter (

smoothing).yt – τt = ct.

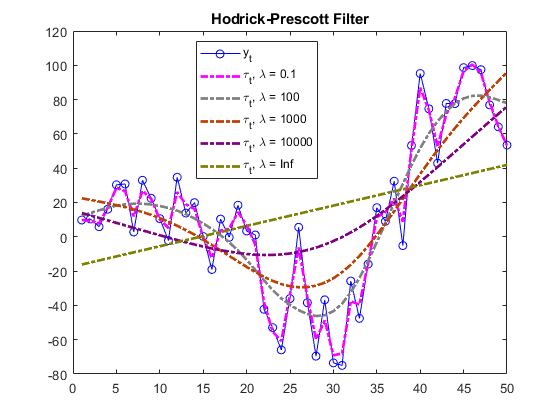

The programming problem is to minimize the objective function over τ1,…,τT. The objective penalizes the sum of squares for the cyclical component with the sum of squares of second-order differences for the trend component (trend acceleration penalty). If λ = 0, the minimum of the objective is 0 with τt = yt for all t. As λ increases, the penalty for a flexible trend increases, resulting in an increasingly smoother trend. When λ is arbitrarily large, the trend acceleration approaches 0, resulting in a linear trend.

This figure shows the effects of increasing the smoothing parameter on the trend component for a simulated series.

The filter is equivalent to a cubic spline smoother, where the smoothed component is τt.

Tips

Hodrick and Prescott [1] suggest values for the smoothing parameter λ (

Smoothing) that depend upon the periodicity of the data, and Ravn and Uhlig [3] suggest adjustments to those values. This table contains their suggested smoothing parameter values for several data periodicities.Periodicity Hodrick and Prescott Suggested SmoothingRavn and Uhlig Suggested SmoothingYearly 100 6.25 Quarterly 1600 1600 Monthly 14400 129600 Supply a vector of smoothing parameters for the

Smoothingname-value argument to test alternatives. Plot the results to visually compare the alternatives.The default two-sided filter (see

FilterType) uses future values of the input series to compute outputs at time t. Because the filter is typically applied to historical data, the results can contain anomalous end effects unsuitable for forecasting [4]. The one-sided filter, by contrast, is causal because it uses only current and previous values of the input series. As a result, the one-sided filter does not revise outputs when new data becomes available.

Algorithms

hpfilter implements the closed-form solution in [2], Appendix A to the original Hodrick-Prescott programming problem [1].

Therefore, hpfilter requires complete data and removes

NaN values in the input data by using listwise deletion.

References

[1] Hodrick, Robert J., and Edward C. Prescott. "Postwar U.S. Business Cycles: An Empirical Investigation." Journal of Money, Credit and Banking 29, no. 1 (February 1997): 1–16. https://doi.org/10.2307/2953682.