Market Risk

Value-at-risk (VaR) and expected shortfall (ES) are important measures of financial risk. VaR is an estimate of how much value a portfolio can lose in a given time period with a given confidence level. ES is the expected loss on days when there is a VaR failure. VaR and ES backtesting tools assess the accuracy of VaR and ES models.

Categories

- Estimate VaR and ES Values

Calculate value-at-risk (VaR) and expected shortfall (ES) for portfolio returns distributions

- VaR Backtest

Create a VaR (value-at-risk) backtest model and run suite of VaR backtests

- Expected Shortfall Backtest

Create an expected shortfall (ES) backtest model and run suite of ES backtests

Featured Examples

Value-at-Risk Estimation and Backtesting

Estimate Value-at-Risk (VaR) and then use backtesting to measure the accuracy of the VaR calculation.

Expected Shortfall Estimation and Backtesting

Perform estimation and backtesting of Expected Shortfall models.

Modeling Tail Data with the Generalized Pareto Distribution

Fit tail data to the Generalized Pareto distribution by maximum likelihood estimation.

Estimate VaR for Equity Portfolio Using Parametric Methods

Estimate the value-at-risk (VaR) for a portfolio of equity positions using two parametric methods, normal VaR and exponentially weighted moving average (EWMA) VaR. Parametric VaR methods, also known as variance-covariance methods when the returns are normally distributed, assume a closed form for the return distribution of the portfolio. Using a parametric model simplifies the problem of VaR calculation to that of estimating the parameters of the distribution. Parametric methods are often contrasted with nonparametric approaches, such as Monte Carlo VaR or historical VaR, that do not assume an analytic formula for the return distribution of the portfolio. For a similar example of VaR calculation on a single index, see Value-at-Risk Estimation and Backtesting.

Estimate Expected Shortfall for Asset Portfolios

Compute the expected shortfall (ES) for a portfolio of equity positions. ES is a market risk metric that supplements a calculated value-at-risk (VaR) value. For an example of ES computation on a single market index, see Expected Shortfall Estimation and Backtesting. The 95% VaR represents the threshold loss amount that is only violated about 5% of the time, while ES is an estimate of the average amount of money the portfolio loses on the 5% of days when the VaR is violated.

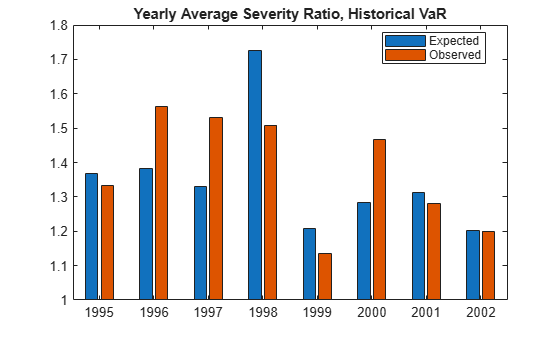

Historical Value-at-Risk Estimation with US Treasury Bonds

Estimate the value at risk (VaR) for a portfolio of US Treasury bonds by using both the historical and filtered historical VaR methods. While this example uses treasury bonds as a typical asset type, you can apply this workflow to any fixed-rate bond with similar par yield data.

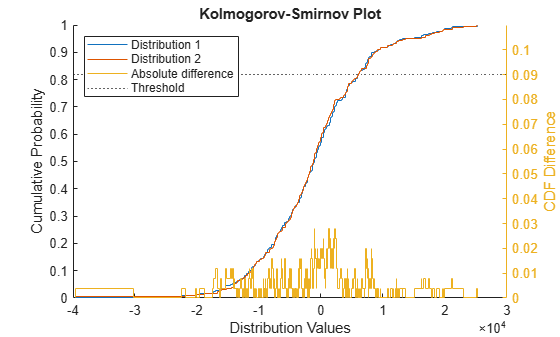

Perform Profit-and-Loss Attribution Test

Apply the Fundamental Review of the Trading Book (FRTB) profit-and-loss (P&L) attribution test to the recent trading history of a portfolio. The P&L attribution test determines whether two empirical distributions containing different P&L measures are similar enough for the measures to be considered equivalent for regulatory purposes. One distribution contains risk theoretical P&L (RTPL) values, which are the portfolio losses calculated by the trading desk's internal valuation model at the end of the trading period. The other distribution contains hypothetical P&L (HPL) values, which are the losses the portfolio would realize if the portfolio did not buy or sell any assets over the trading period. Profits are represented by negative P&L values.