mvtpdf

Multivariate t probability density function

Syntax

Description

Examples

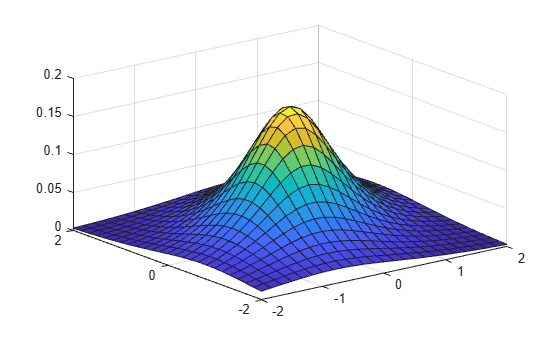

Compute the pdf of a multivariate t distribution with the correlation parameters C=[1 .4; .4 1] and 2 degrees of freedom.

[X1,X2] = meshgrid(linspace(-2,2,25)',linspace(-2,2,25)'); X = [X1(:) X2(:)]; C = [1 .4; .4 1]; df = 2; p = mvtpdf(X,C,df);

Plot the pdf.

figure; surf(X1,X2,reshape(p,25,25))

Input Arguments

Output Arguments

Version History

Introduced in R2006b